When you refinance your mortgage, you get to pick your loan term all over again. And the choice between a 15-year and a 30-year mortgage is one of the biggest financial decisions you can make.

The good news: there's no single right answer. The right choice depends on your income, your monthly budget, your goals, and how long you plan to stay in your home.

This article breaks down the difference between the two options in plain terms — and shows you how to figure out which one actually makes sense for your situation.

The Basic Difference

A 30-year mortgage spreads your loan out over 360 months. Because the payments are stretched out over a longer time, each monthly payment is lower — but you're paying interest for 30 years.

A 15-year mortgage pays off the loan in 180 months. Your monthly payment is higher — but you pay far less interest over the life of the loan, and you build equity much faster.

Think of it this way: the 30-year gives you breathing room in your monthly budget. The 15-year gets you out of debt faster and costs less overall.

What the Numbers Actually Look Like

Here's a simple example to make this real.

Say you're refinancing a $300,000 mortgage at a rate of 6.5% on a 30-year loan vs. 6.0% on a 15-year loan. (15-year loans typically come with a slightly lower interest rate because the lender's risk is shorter.)

| 30-Year | 15-Year | |

|---|---|---|

| Monthly Payment | ~$1,896 | ~$2,532 |

| Total Interest Paid | ~$382,600 | ~$155,800 |

| Difference | — | Save ~$226,800 in interest |

The 15-year payment is about $636 more per month. But you save over $226,000 in interest by the time the loan is paid off.

That's a huge number. But so is $636 extra per month. Which is why this isn't a simple "one is always better" conversation.

Why People Choose the 30-Year

The 30-year mortgage is the most popular choice for a reason: lower monthly payment.

That lower payment gives you more flexibility. If something unexpected happens — job loss, medical bills, a major repair — you're not locked into a high payment you can't make.

It also frees up cash each month that you could use to:

• Build up your emergency fund

• Invest in a retirement account

• Put toward other financial goals

• Pay off higher-interest debt (like credit cards)

If you invest the difference between a 30-year and 15-year payment — and your investments earn more than your mortgage interest rate — you could theoretically come out ahead financially, even paying more in mortgage interest.

A 30-year mortgage also makes sense if your income is variable (freelancers, commission workers, business owners) and you want the minimum required payment to stay manageable.

Why People Choose the 15-Year

The 15-year mortgage is a powerful tool for people who want to own their home free and clear as fast as possible and don't mind the higher payment.

The advantages are real:

• Lower interest rate — lenders typically offer better rates on 15-year loans

• Massive interest savings — you could save six figures in total interest

• Faster equity growth — more of every payment goes toward principal from the start

• You're done in 15 years — if you're 50, you could be mortgage-free by 65

The 15-year is especially appealing to homeowners who are further along in their careers, have stable incomes, and want to have their home paid off before retirement.

When Debt Consolidation Makes the 15-Year Even More Compelling

Here's a scenario that surprises a lot of people.

Imagine you're carrying a $20,000 credit card balance at 22% interest and a $15,000 car loan at 8%. Your combined monthly payments on those two debts might be $900 or more — on top of your existing mortgage payment.

Now imagine doing a cash-out refinance that rolls all of that debt into your new mortgage and pays it off completely.

Even if you choose a 15-year term — which has a higher monthly payment than a 30-year — your total monthly obligations (mortgage + all debt payments combined) may actually go down. You've replaced $900/month in consumer debt with a slightly higher mortgage payment, but at a much lower interest rate.

That's the key: mortgage rates are typically far lower than consumer debt rates. Credit cards charge 20–25% interest. Car loans often run 6–10%. Even a mortgage at 7% is a dramatically better deal than the debt you're replacing.

When you consolidate high-interest debt into a cash-out refinance:

• You're trading 20%+ credit card interest for a mortgage rate that's a fraction of that

• You're replacing multiple minimum payments with one predictable monthly payment

• You're turning unsecured consumer debt (which builds no asset) into mortgage debt (which builds equity in your home)

And when you pair that with a 15-year term, you're not just getting a better rate — you're also committing to pay everything off faster, which means even less total interest paid over time.

The math doesn't always work out this way. It depends on how much debt you're carrying, how much equity you have in your home, and the rate you can qualify for. But for homeowners sitting on significant high-interest debt, a 15-year cash-out refinance is often worth modeling before defaulting to a 30-year.

Run the numbers on your situation → https://shouldirefi.app/tool/calculator

The Hidden Factor: Where Are You Now in Your Current Loan?

Here's something a lot of people miss when thinking about refinancing: how far along are you in your current loan?

If you're 10 years into a 30-year mortgage, you only have 20 years left. Refinancing into a new 30-year loan doesn't just change your rate — it resets your clock back to 30 years.

That means you'd be paying for a total of 40 years instead of 30. Even if the new rate is lower, you could end up paying more in total interest because you've added a decade back on.

In cases like this, refinancing into a 15-year loan (or even a 20-year loan) might get you a better rate and keep your payoff timeline closer to where you were.

This is one of the most important questions to ask before refinancing: not just "what's my new rate?" but "how does the total interest compare?"

Making Extra Payments: A Middle Path

One option many homeowners don't consider: get the 30-year, but make extra payments when you can.

This gives you the flexibility of a lower required payment — which protects you if money gets tight — while still allowing you to pay the loan off faster in good months.

If you consistently pay an extra $300–$500 per month on a 30-year mortgage, you could pay it off years early and save a significant amount in interest without being locked into the higher payment required on a 15-year.

The catch: this requires discipline. Some people do better with the forced savings of a 15-year. Others appreciate the flexibility.

Which One Is Right for You?

Here's a simple way to think about it:

Choose the 30-Year if:

• The higher 15-year payment would strain your monthly budget

• You have other high-interest debt to pay off first

• Your income is variable and you want flexibility

• You want to invest the difference instead of paying down the mortgage

Choose the 15-Year if:

• You can comfortably afford the higher payment without stress

• You're closer to retirement and want to own your home outright

• You've already paid off most other high-interest debt

• Peace of mind from owning your home free and clear matters to you

There's no formula that spits out a perfect answer. But running the actual numbers for your situation gets you a lot closer.

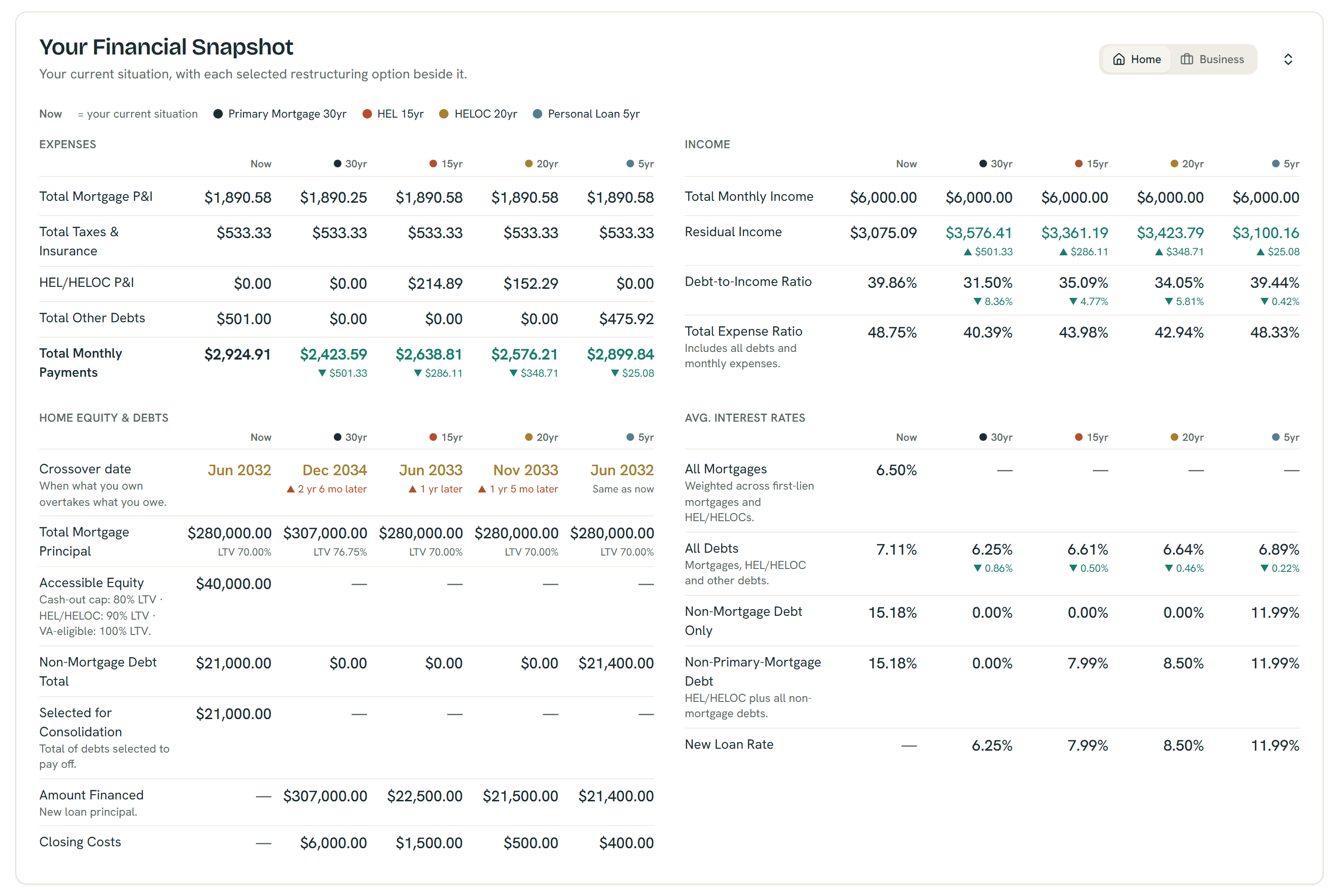

The Financial Snapshot puts every option beside your current numbers — example figures shown; all outputs are estimates, not quotes or offers.

See the Full Picture for Your Numbers

The best way to make this decision is to model both options side by side with your real numbers — your current balance, the rate you're being offered, your monthly budget, and how long you plan to stay in the home.

Try the ShouldIRefi Calculator → https://shouldirefi.app/tool/calculator

The calculator lets you compare a 15-year vs. 30-year refinance scenario directly. You'll see:

• Monthly payment for each option

• Total interest paid over the life of each loan

• Break-even point (how long until savings cover closing costs)

• Equity growth over time under each scenario

You can also toggle on the "extra payment" feature to model what happens if you take the 30-year but make extra payments each month — so you can see exactly how many years that would shave off and how much interest it would save.

Start for free → https://shouldirefi.app/tool/calculator

Not sure what numbers to enter? Start with the Financial Audit https://shouldirefi.app/tool/audit— it walks you through your full picture step by step and loads everything into the calculator automatically.