If you’ve been shopping for a mortgage or thinking about refinancing, you’ve probably seen two main options: a fixed-rate mortgage and an adjustable-rate mortgage (ARM). Right now, more people are picking ARMs than at any point in the last three years.

Is that smart? Or are they setting themselves up for a nasty surprise?

The honest answer is: it depends. And the right choice for you comes down to a few key questions about your life and your numbers.

First, What’s the Difference?

A fixed-rate mortgage locks in your interest rate for the entire life of the loan. Your payment stays the same every month — whether you have the loan for 5 years or 30. No surprises.

An adjustable-rate mortgage (ARM) starts with a lower fixed rate for a set period — usually 5, 7, or 10 years — and then adjusts based on market conditions after that. The most common type is a 5/1 ARM: fixed for 5 years, then adjusts once per year after that.

Right now, a 30-year fixed rate is hovering around 6.5%. A 5/1 ARM might open at around 5.3–5.5%. That’s a meaningful gap — and it’s why ARMs are getting popular again.

Why ARMs Are Getting Popular Right Now

When rates are low and stable, there’s not much reason to take on the risk of an ARM. A fixed rate at 3% is already great — why gamble?

But when rates are higher, the lower initial rate on an ARM becomes more attractive. A 1–1.25% gap in rate can save a homeowner with a $400,000 loan $200–$300 a month during the fixed period. Over 5–7 years, that’s real money.

On top of that, many people believe rates will drop over the next few years. If they’re right, and rates fall before the ARM starts adjusting, an ARM owner could refinance into a lower fixed rate — and get the best of both worlds.

That’s the theory. Now let’s look at the risk.

When an ARM Makes Sense

An ARM is a reasonable choice in specific situations. Here are the clearest ones:

1. You’re fairly certain you’ll move or sell before the fixed period ends.

If you know you’re moving in 4–5 years — job change, growing family, retirement — you’ll likely sell the home before your ARM ever adjusts. You lock in the lower rate, save money for years, and walk away. The risk of rate adjustment never actually hits you.

2. You expect rates to fall significantly before your adjustment kicks in.

If you take a 7/1 ARM today and rates drop over the next few years, you can refinance into a lower fixed rate before your ARM even starts adjusting. You’d get a lower rate now AND a lower fixed rate later.

3. You expect your income to grow.

Some borrowers — like people early in their career — choose an ARM because they want the lower payment now, knowing their income will be higher by the time the rate adjusts. If the payment rises in 5 years, they’ll be earning more to handle it.

When a Fixed Rate Is the Smarter Move

1. You plan to stay in the home long-term.

If you’re buying your forever home — or expect to be there 10+ years — locking in a fixed rate removes all uncertainty. You know exactly what your payment will be. If rates rise, you’re protected. If rates fall, you can always refinance later.

2. Your budget is already stretched.

A higher payment in year 6 could be a real problem if your budget is tight. ARMs are harder to manage if you don’t have room for the payment to increase. Fixed rates give you the stability to plan around a number that won’t change.

3. You want to plan without the guesswork.

Some people just don’t want to think about when to refinance, what rates will do, or whether they’ll still be in the house in 7 years. That’s completely valid. A fixed rate removes the decision entirely.

The Real Risk: What Happens When Your ARM Adjusts

This is the part most people gloss over — and it’s the most important.

After the fixed period ends, your ARM rate adjusts based on a market index plus a margin set by your lender. Most ARMs have caps that limit how much the rate can go up each year and over the life of the loan. A common structure is:

• First adjustment cap: Rate can’t jump more than 2% in the first adjustment

• Per-year cap: Rate can’t rise more than 2% per year after that

• Lifetime cap: Rate can’t rise more than 5% above the starting rate over the life of the loan

So if your 5/1 ARM started at 5.5%, the most it could ever reach is 10.5% — even if market rates skyrocket.

That said, even a 2% jump in year 6 would meaningfully raise your payment. On a $400,000 loan, going from 5.5% to 7.5% could add $400–$500 per month. If you haven’t planned for that, it’s a shock.

The key question: Can you afford the payment at the maximum possible rate? If the answer is yes — and you have a plan for what happens at year 5 — an ARM is manageable. If the answer is no, fixed is safer.

ARM vs. Fixed: How to Actually Compare Them for Your Situation

The difference between a good ARM decision and a bad one isn’t which type of loan is “better” — it’s whether you’ve done the math for your specific numbers.

Here’s what to actually compare:

1. Total interest paid over the period you expect to stay in the home — not just monthly payment

2. How long it takes to break even on any refinance you might do during or after the ARM period

3. What your payment looks like at the cap rate — make sure you can handle the worst case

4. Whether paying the lower ARM rate now and refinancing later saves more than locking in a fixed rate today

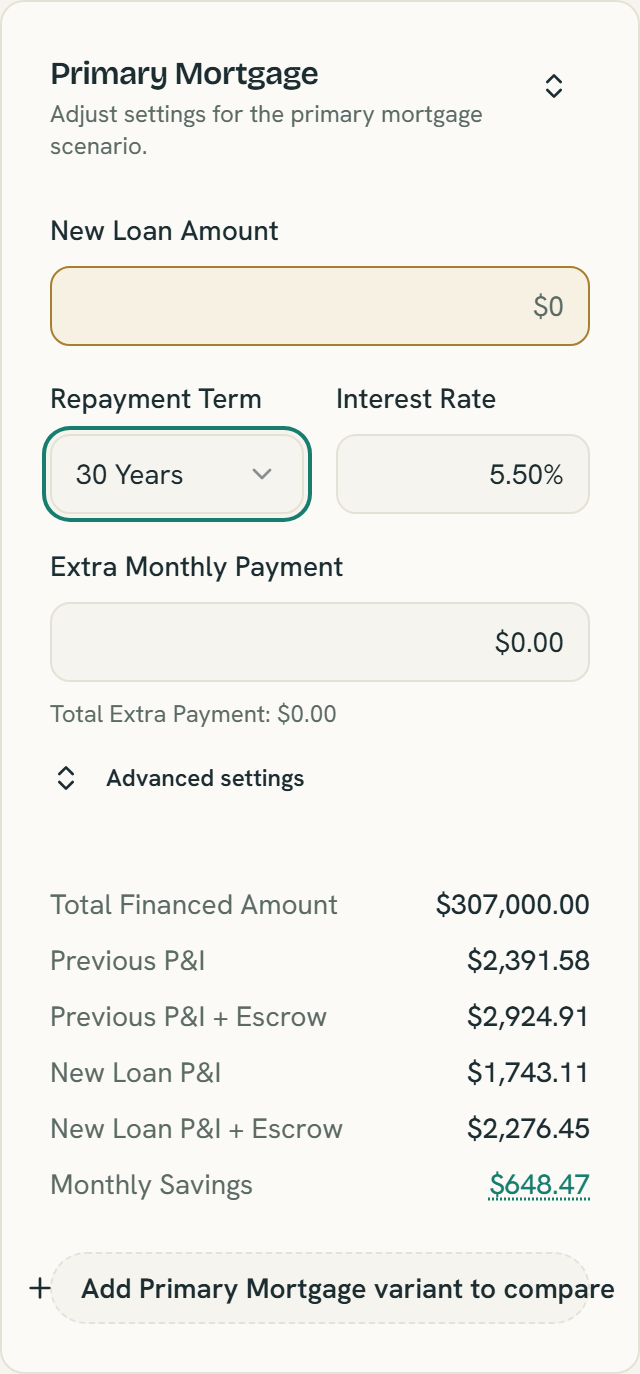

These comparisons are exactly what a side-by-side scenario tool is built for. You can enter both loan options and see total interest, monthly payment, and equity projections side by side — instantly.

Model both options in the ShouldIRefi Calculator → https://shouldirefi.app/tool/calculator

Enter your loan amount, run it with a 5/1 ARM rate on one side and a 30-year fixed on the other. Adjust the timeline to match how long you actually expect to stay. The calculator shows you total interest paid, break-even projections, and 30-year equity under each scenario.

You can also save both scenarios and come back when rates change.

Try it free → https://shouldirefi.app/tool/calculator

Or if you want a guided walkthrough of your full financial picture, start with the Financial Audit _https://shouldirefi.app/tool/audit_— it loads all your details into the calculator automatically.

Scenario settings show the payment math as you type — example figures; estimates only, not an offer. ARM mode with rate caps lives under Advanced settings.

The Bottom Line

ARMs are not inherently risky or bad. Fixed rates are not inherently better. Both are tools — and the right one depends on your timeline, your budget, and how much uncertainty you’re comfortable with.

The dangerous move is choosing without running the numbers.