If you own a home, you may have heard these three terms thrown around: cash-out refinance, HELOC, and home equity loan. They all let you use the value of your home to get money — but they work in very different ways. Choosing the wrong one could cost you thousands of dollars.

This guide breaks down each option in simple terms, shows you when each one makes sense, and helps you figure out where to start.

What Do These Three Options Have in Common?

All three let you borrow against your home equity — the portion of your home that you actually own. For example, if your home is worth $300,000 and you still owe $200,000 on your mortgage, you have $100,000 in equity.

Lenders usually let you borrow up to 80% of your home's value. That means your loan balance plus any new money you borrow can't go over that limit in most cases.

Because your home is used as collateral, all three options typically come with lower interest rates than credit cards or personal loans. But they also come with risk: if you stop making payments, you could lose your home.

Option 1: Cash-Out Refinance

A cash-out refinance replaces your current mortgage with a brand-new, larger one. The difference between your old mortgage and your new one is paid to you in cash at closing.

Example: You owe $200,000 on your mortgage. You refinance for $260,000. After closing costs, you walk away with roughly $60,000 in cash — and now have one new monthly mortgage payment.

Best for:

- Getting a large lump sum of money

- Locking in a fixed interest rate

- Possibly lowering your mortgage rate at the same time

- Simplifying to one monthly payment

Watch out for:

- Closing costs, which can be 2–5% of the loan amount

- If rates are higher now than when you got your original mortgage, your payment could go up

- Your loan term resets, which could mean more interest paid over time

Option 2: HELOC (Home Equity Line of Credit)

A HELOC works more like a credit card. You're approved for a certain amount, and you can borrow from it, pay it back, and borrow again — all during what's called the draw period, which usually lasts about 10 years.

After the draw period ends, you enter the repayment period (usually another 10–20 years), where you pay back what you borrowed plus interest.

A HELOC does not replace your existing mortgage. It's a second loan on top of it.

Payments during the draw period: This is something a lot of borrowers miss — a HELOC isn't payment-free while you're drawing from it. During the draw period, you're typically required to make a monthly payment. That payment is usually interest-only, calculated on only the amount you've currently borrowed (not your full credit limit). So if your limit is $80,000 but you've only pulled out $20,000, your payment is based on that $20,000 balance.

Some HELOCs do require principal and interest payments during the draw period, depending on the lender. Either way, once the draw period ends and the repayment period begins, your monthly payment increases — often significantly — because you're now paying down the principal balance on a fixed schedule.

Best for:

- Ongoing expenses, like a home renovation that happens in stages

- Keeping your current mortgage rate untouched

- Flexibility — borrow only what you need, when you need it

- Lower upfront closing costs

Watch out for:

- Most HELOCs have variable interest rates, so your payment can go up or down over time

- You'll have two monthly payments instead of one (your existing mortgage plus the HELOC)

- Your payment can jump sharply when the repayment period starts, since you're now paying down principal

- It may be tempting to overborrow since it works like a credit card

Option 3: Home Equity Loan (HEL)

A home equity loan is also a second mortgage — meaning it doesn't touch your existing loan. But unlike a HELOC, you receive all the money upfront in one lump sum, and you pay it back in fixed monthly payments over a set term (usually 5 to 30 years).

Think of it as a HELOC with training wheels — you know exactly what you're borrowing and exactly what you'll pay each month.

Best for:

- One-time expenses where you know exactly how much you need

- Preferring a fixed rate and predictable payment

- Keeping your original mortgage rate intact

Watch out for:

- Interest rates are usually a little higher than a cash-out refinance, since it's a second lien

- Less flexibility than a HELOC — you can't reborrow once it's repaid (without getting a new loan)

- Still comes with closing costs, though usually less than a full refinance

Side-by-Side Summary

| Cash-Out Refi | HELOC | Home Equity Loan | |

|---|---|---|---|

| Replaces your mortgage? | Yes | No | No |

| How you get the money | Lump sum | As needed (revolving) | Lump sum |

| Interest rate type | Fixed | Usually variable | Fixed |

| Monthly payments | One (replaces old mortgage) | Two (existing + HELOC) | Two (existing + HEL) |

| Closing costs | Higher | Lower | Moderate |

| Best for | Large one-time need + rate opportunity | Ongoing or flexible spending | One-time need, keep current rate |

So Which One Is Right for You?

Here's a simple way to think about it:

- If you can get a lower rate than your current mortgage and need a large sum — a cash-out refi often makes the most sense.

- If your current mortgage rate is already low and you don't want to lose it — a HELOC or home equity loan keeps it untouched.

- If you need money over time (not all at once) — a HELOC gives you that flexibility.

- If you want a second loan with predictable payments — a home equity loan is the more stable option.

The tricky part is that the "right" answer depends on your specific numbers — your current rate, your home value, how much debt you have, and what you're trying to accomplish.

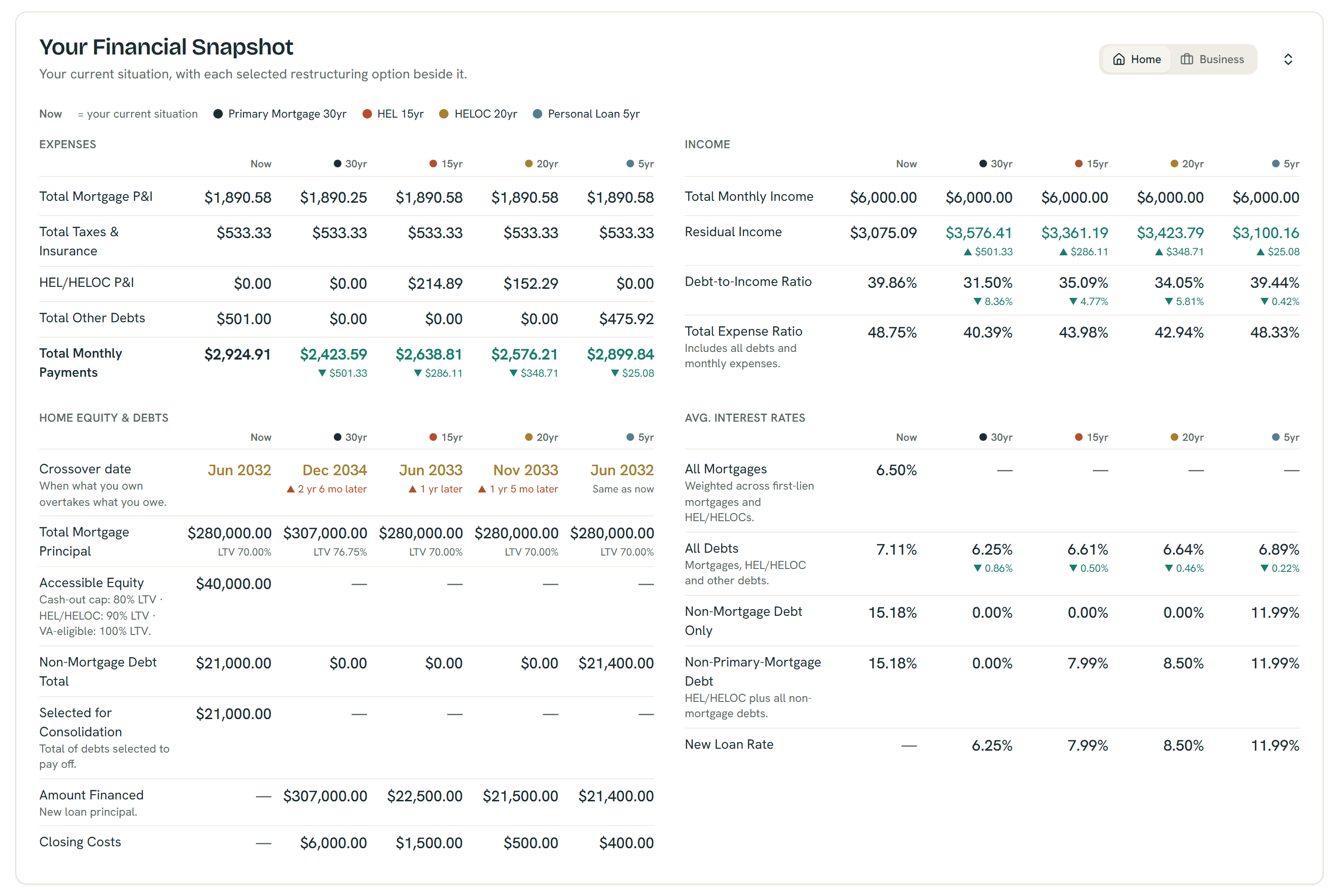

The Financial Snapshot puts every option beside your current numbers — example figures shown; all outputs are estimates, not quotes or offers.

See Your Real Numbers in Minutes

Reading about options is a great start. But every situation is different — and the only way to know which option actually saves you the most is to run your own numbers.

Try the ShouldIRefi Calculator → (https://shouldirefi.app/tool/calculator)

You can model a cash-out refinance, HELOC, and home equity loan side by side — and instantly see which one saves you more money, lowers your monthly payment the most, or builds equity the fastest. It's free to use and takes just a few minutes.

Not sure where to start? Take the Financial Audit → (https://shouldirefi.app/tool/audit) — it walks you through your full financial picture step by step and loads everything into the calculator for you.