A lot of debt consolidation articles assume you own a home. They talk about cash-out refinances, HELOCs, and home equity loans — all great tools, but all off the table if you don't have a home and equity to borrow against.

If you're renting, or you simply don't have meaningful home equity, this article is for you. There are real options for consolidating debt without owning property — and some of them can save you a lot of money.

Why People Consolidate Debt

Carrying multiple debts — credit cards, auto loans, student loans, personal loans — means multiple due dates, multiple minimum payments, and often multiple high interest rates. Consolidation combines them into a single loan with one payment, and ideally a lower interest rate.

The goal isn't just simplicity. It's saving money on interest and getting out of debt faster.

Option 1: Personal Loan (Unsecured)

A personal loan is the most accessible debt consolidation tool for people without home equity. You borrow a set amount, use it to pay off your other debts, and repay the personal loan in fixed monthly payments over a set term — typically 2 to 7 years.

What makes it useful for renters:

- No home equity required

- Your home (or anything else) is not used as collateral

- Fixed rate and fixed payment — no surprises

- Can borrow up to $100,000 depending on your credit and income

- Funds often available in 1–2 business days

What to know:

- Interest rates are higher than home equity products, because there's no collateral

- Rates vary significantly by credit score — better credit = better rate

- Some lenders charge origination fees (typically 1–8% of the loan amount)

If you can get a personal loan rate that's meaningfully lower than what you're currently paying on your credit cards or other debts, consolidation can make a real financial difference.

Option 2: Balance Transfer Credit Card

Some credit cards offer a 0% introductory APR for a set period — typically 12 to 21 months — for balances transferred from other cards. If you can pay off the debt entirely within that window, you save all the interest you'd otherwise pay.

What makes it useful:

- Potentially 0% interest for over a year

- Can make a significant dent in debt if you're aggressive about paying it off

What to watch out for:

- You typically need very good credit to qualify

- There's usually a balance transfer fee of 3–5%

- After the intro period ends, the regular APR kicks in — and it's often high

- Only works for credit card debt (not auto loans, student loans, etc.)

Option 3: DIY Strategies (No New Loan Required)

If your credit isn't strong enough to qualify for a better rate, or if you prefer to avoid new debt, structured payoff strategies — like the snowball or avalanche methods — can still dramatically reduce your total interest and get you out of debt faster. No loan needed.

What Renters Often Don't Realize

Many debt consolidation articles focus exclusively on homeowners, which can leave renters thinking their options are limited. They're not.

A personal loan can consolidate credit cards, auto loans, student loans, and other debts into one payment at a potentially lower rate — all without collateral, without a mortgage, and without putting anything at risk.

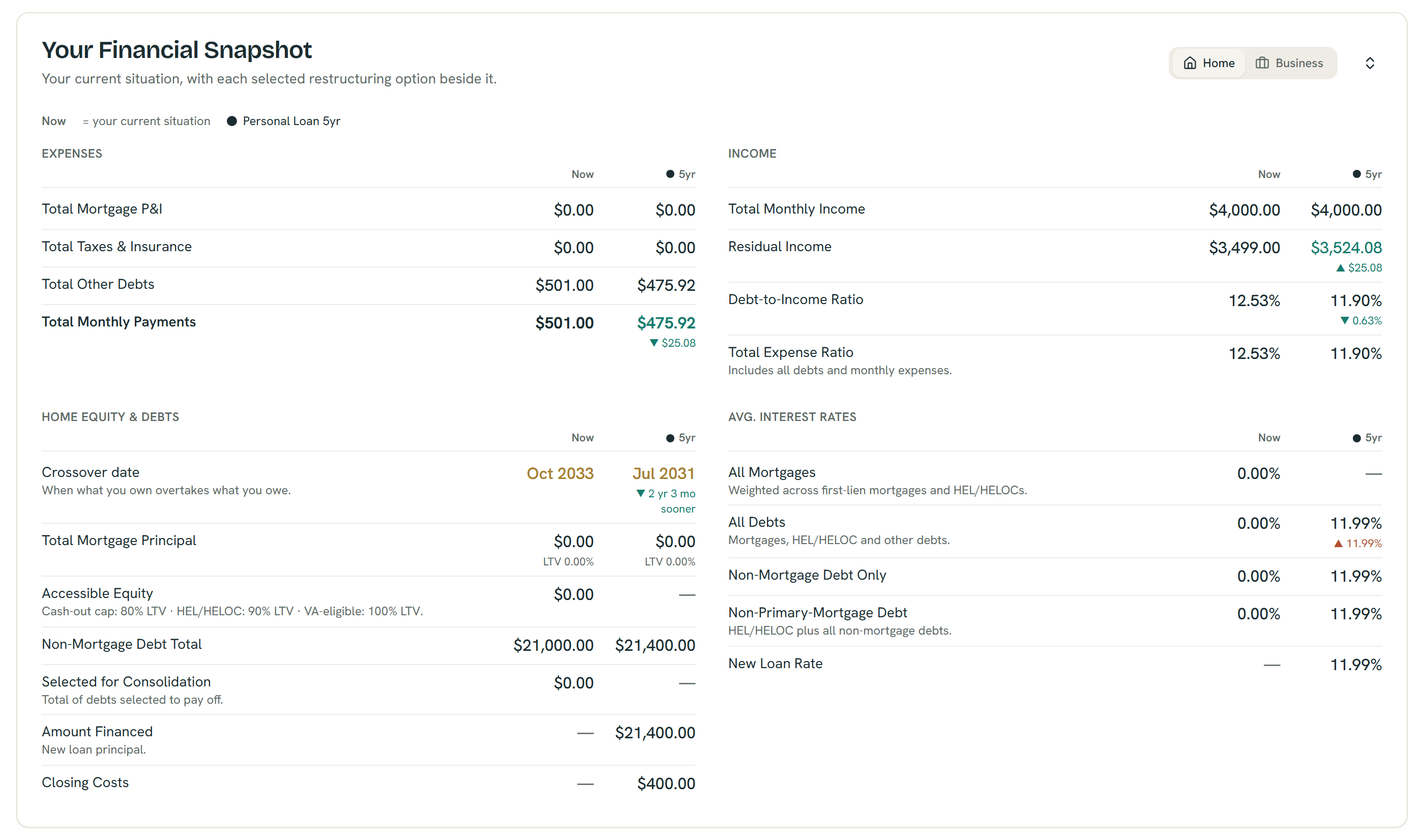

No home required: the same side-by-side comparison works for renters — example figures; estimates only.

Compare Your Options Before You Borrow

Whether you're a renter or a homeowner, the key is running the actual numbers before committing to anything. The right loan term, the right rate, and the right monthly payment depend on your specific situation.

Try the ShouldIRefi Calculator → (https://shouldirefi.app/tool/calculator)

The calculator works for renters and non-homeowners too. Skip the property fields and enter your debts and income — the app automatically shows the personal loan and self-pay options available to you. You can compare:

- Your current situation (minimum payments, total interest, payoff timeline)

- A personal loan scenario (at a rate and term you choose)

- A self-pay strategy with extra monthly payments

You'll see exactly which approach gets you out of debt fastest and for the least money.

Try it free → (https://shouldirefi.app/tool/calculator)

Not sure where to start? Take the Financial Audit (https://shouldirefi.app/tool/audit) — it's designed for renters and homeowners alike, and loads your full financial picture into the calculator automatically.