Debt has a way of feeling like a fog — always there, hard to see through, and easy to lose your bearings in. Most people with multiple balances know they need a plan, but fewer know that the order in which you pay down debt can mean the difference between thousands of dollars saved and thousands more handed over to lenders.

The good news: there are proven strategies for this, and you don't have to guess which one is best for your specific situation. You can model it.

Why Strategy Matters More Than Willpower

The most common debt payoff mistake isn't a lack of motivation — it's throwing extra money at debt randomly. Making larger payments is always better than making minimums, but where you put those extra dollars changes the math significantly.

Different debts compound differently. A $5,000 balance at 24% is costing you exactly $100 per month in interest — before you've paid a single dollar of principal. A $12,000 balance at 6% costs you $60 per month. Paying down the smaller balance first feels faster, but it leaves the more expensive debt compounding the whole time.

Understanding the mechanics behind each strategy helps you choose deliberately rather than by feel.

The Four Main Debt Payoff Strategies

1. The Debt Avalanche (Highest Interest First)

The avalanche method is mathematically optimal. You make minimum payments on every debt, then put every extra dollar toward the balance with the highest interest rate. Once that's paid off, you "roll" that entire payment into the next-highest-rate debt — and so on, until you're debt-free.

Why it works: By eliminating the most expensive debt first, you stop the most damaging interest from compounding. Over time, you pay less total interest and often get out of debt faster than any other self-pay approach.

The tradeoff: If your highest-rate debt also has a large balance, it might take a long time before you see your first account close. That can feel discouraging, especially early in the process.

Best for: People who are motivated by the numbers and have the discipline to stick with a plan even when visible progress is slow.

2. The Debt Snowball (Smallest Balance First)

The snowball method flips the logic: you ignore interest rates and target the smallest balance first. Once that debt is gone, the payment you were making on it gets rolled into the next-smallest debt. Your payment amounts grow — like a snowball — as you eliminate accounts.

Why it works: Behavioral research consistently shows that clearing individual accounts, even smaller ones, creates psychological momentum that keeps people on plan longer. Fewer accounts to manage also means fewer payments to track, which reduces the chances of a missed payment.

The tradeoff: Because you're not targeting high-interest debt first, you'll likely pay more in total interest compared to the avalanche method — sometimes significantly more if there's a large rate spread between your balances.

Best for: People who need quick wins to stay motivated, or who have several small balances that feel overwhelming.

3. Debt Consolidation via Personal Loan

Consolidation is a different kind of strategy. Instead of choosing an order to pay off existing debts, you replace multiple debts with a single personal loan — ideally at a lower interest rate than your current weighted average.

Why it works: If you're carrying debt at a blended rate well above what a personal loan would cost, you immediately reduce the rate at which interest accrues. You also simplify your finances: one payment, one due date, one lender. A fixed repayment term gives you a clear finish line.

The tradeoff: Consolidation only helps if your new loan rate is genuinely lower than what you're currently paying on a blended basis. Extending your loan term to lower the monthly payment can also cost you more in total interest even if the rate is lower — the math depends on the specifics.

Best for: People with multiple high-rate balances who qualify for meaningfully better rates and want to simplify repayment into a single fixed monthly payment.

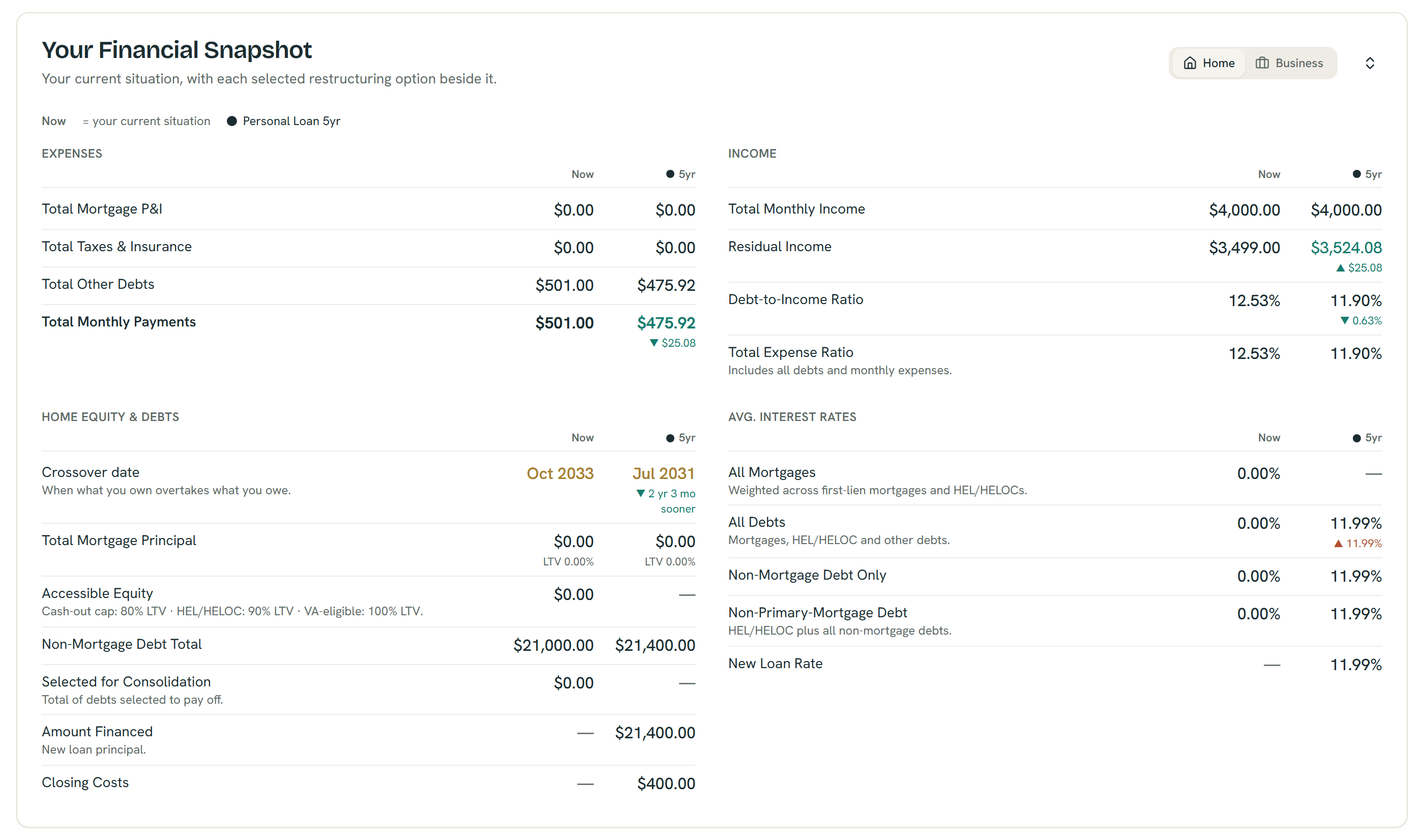

Try it in the ShouldIRefi Calculator: Enter your current debts, then add a personal loan scenario. The calculator will show you your monthly payment under the new loan versus your current situation, total interest paid, and your debt-to-income ratio before and after. You can see exactly whether consolidation is worth it for your numbers.

4. Self-Pay with Accelerated Payments

This is the most straightforward approach: keep your current debts as-is, but add extra payments each month on top of minimums. You can combine this with either the avalanche or snowball ordering above.

The key variable here is consistency. Even a modest extra payment can shave significant time off your payoff timeline and save real money in interest — how much depends on which debt you target and how high its rate is.

Why it works: No new loan, no closing costs, no credit inquiry. Just redirecting cash flow you already have toward faster paydown.

The tradeoff: It requires identifying where the extra money comes from. If your budget is already tight, there may not be much room. It also requires discipline over a longer runway than consolidation.

Best for: People who have consistent monthly cash flow above their minimums, don't want to take on new debt, and want to avoid fees.

Try the Self-Pay option in the ShouldIRefi Calculator: The Self-Pay scenario lets you add an extra monthly payment and see exactly how many months it cuts off your payoff timeline and how much interest you avoid. You can toggle the "Snowball to mortgage" feature if you're a homeowner — or simply see how your debt balances shrink over time.

A Fifth Option Worth Knowing: The Invest-vs-Pay-Off Decision

Once you've decided how to pay off debt, a natural follow-on question is whether to put every spare dollar toward debt — or whether some of that money might be better off invested.

This is genuinely nuanced, but a useful rule of thumb: if the interest rate on your debt is above the expected return on a given investment, paying down that debt first gives you a more certain, equivalent return. High-rate debt like credit cards almost always wins this comparison — their rates typically far exceed what most investments reliably produce. Lower-rate debt like federal student loans or a mortgage sits in murkier territory, where the comparison between investing and paying down depends on your assumptions about future returns, your tax situation, and your risk tolerance.

Neither choice is wrong — they involve tradeoffs between a guaranteed outcome (eliminating an interest cost) and a probabilistic one (growing invested assets). What matters is that you run the numbers for your actual balances and rates, not a hypothetical.

Model both in the ShouldIRefi Calculator: The investment toggle lets you redirect freed-up cash into a modeled asset instead of debt repayment, so you can compare both paths side by side — not in theory, but with your own numbers.

Hybrid Approaches: When You Don't Have to Pick Just One

No strategy requires total commitment to a single method. And in some situations, a thoughtfully constructed hybrid can outperform both the snowball and the avalanche — in total interest paid, time to debt freedom, and monthly financial flexibility.

Here's a worked example using real amortization math.

The Hybrid in Action: A Side-by-Side Comparison

Starting situation:

| Debt | Balance | APR | Min. Payment |

|---|---|---|---|

| Credit Card A | $3,500 | 15.99% | $88/mo |

| Credit Card B | $8,500 | 24.99% | $213/mo |

| Auto Loan | $9,000 | 7.50% | $200/mo |

| Total | $21,000 | 15.99% weighted avg | $501/mo |

The person has $150/mo available beyond their minimums — a total monthly outflow of $651.

Strategy A — Snowball (CC A first, then CC B, then Auto):

CC A is the smallest balance, so it gets the extra $150. It's paid off at month 18. The freed $238/mo ($88 min + $150 extra) rolls into CC B, which closes at month 40. Everything then piles onto the auto loan, which is paid off at month 44.

- Total interest paid: $6,792

- Months to debt-free: 44

- Required monthly minimum: $501

Strategy B — Avalanche (CC B first, then CC A, then Auto):

CC B has the highest rate at 24.99%, so the extra $150 goes there. CC B closes at month 33. The freed $363/mo rolls into CC A, which closes at month 38. Auto closes at month 42.

- Total interest paid: $6,016

- Months to debt-free: 42

- Required monthly minimum: $501

The avalanche saves about $777 and finishes 2 months faster than the snowball — a meaningful difference that comes entirely from targeting the higher-rate debt first.

Strategy C — Hybrid: Consolidate + Redirect Savings + Extra Payment

Instead of picking a payoff order, the person consolidates all $21,000 into a single personal loan at 11.99% APR over 60 months. The standard payment on that loan works out to $467/mo — $34 less per month than the combined $501 they were paying in minimums before.

That $34 in savings gets redirected as extra payment on the new loan, along with the original $150. So the effective monthly payment on the loan becomes $651 — the exact same total outflow as before.

| Hybrid Strategy | |

|---|---|

| Consolidation loan amount | $21,000 |

| New APR | 11.99% (down from 15.99% weighted avg) |

| Standard monthly payment | $467 |

| Monthly savings in required obligation | $34 |

| Extra applied (savings + $150 base) | $184 |

| Effective loan payment | $651 |

Result: the loan is paid off in 40 months, with $4,476 in total interest.

| Strategy | Months | Total Interest | Required Monthly Min |

|---|---|---|---|

| Snowball | 44 | $6,792 | $501/mo |

| Avalanche | 42 | $6,016 | $501/mo |

| Hybrid | 40 | $4,476 | $467/mo |

The hybrid pays off the debt 4 months faster than the snowball and 2 months faster than the avalanche, while saving $2,316 vs. the snowball and $1,540 vs. the avalanche in total interest.

And critically: the required monthly obligation drops from $501 to $467. That $34/mo difference might seem small, but it's the amount the person is required to pay — not what they're choosing to pay. In a month where an unexpected expense hits, they have more room to breathe without falling behind. That financial flexibility is baked into the structure, not dependent on discipline.

Why does the hybrid win? By lowering the interest rate on the full $21,000 from the start, it reduces the rate at which every dollar of that balance accrues interest — immediately, not after the first or second debt is paid off. The snowball and avalanche are both working against the original rates for months before they get to attack the high-rate balance in full. The consolidation loan changes the math from day one.

When the Hybrid Works Best

The hybrid approach is most powerful when:

- Your current debt rates are meaningfully higher than what you'd qualify for on a personal loan

- You have multiple debts that would take many months to pay off individually

- You want to reduce your required monthly obligation while still aggressively paying down debt

It's less compelling when your existing rates are already low, when you'd face significant origination fees on the new loan, or when you can't qualify for a rate that's clearly better than your weighted average.

Run the comparison yourself in the ShouldIRefi Calculator: Enter your current debts, then model a personal loan scenario at a lower rate. The calculator will show your monthly payment, total interest, and debt-to-income ratio side by side — so you can see whether consolidation makes sense before committing to anything.

For Student Loan Borrowers: Your Strategy Set Is Different

Federal student loans don't behave like credit cards or personal loans. They have their own income-based repayment options, forgiveness timelines, and rules around forbearance — and choosing the right repayment plan has more impact than most of the ordering decisions above.

The nine federal repayment plans range from fixed 10-year Standard repayment to income-driven options where your monthly payment is calculated as a percentage of your income and any remaining balance is forgiven after 20–30 years.

If you have federal student loans, the most important first move is comparing those plans side by side with your actual balance, income, and family size — because the "best" plan is genuinely different for different people.

Use the ShouldIRefi Student Loan Simulator: When you mark any debt as a student loan, the simulator automatically calculates all nine federal repayment plans at once — monthly payment, total interest, term length, and any forgiven balance at the end. You can toggle forbearance months, add extra payments, and select a plan to compare it directly against other debt payoff options on the main chart.

No home required: the same side-by-side comparison works for renters — example figures; estimates only.

Where to Start: Running Your Own Audit

The hardest part of picking a strategy isn't understanding the options — it's having an accurate picture of where you stand. That means knowing:

- Every debt balance, interest rate, and minimum monthly payment

- Your gross monthly income

- Your monthly expenses outside of debt payments

- Whether you own a home (which opens additional equity-based options)

Without that picture, any strategy is abstract. With it, you can run actual projections.

Start with the ShouldIRefi Financial Audit: It's a guided questionnaire that walks you through your full financial picture — property, debts, income, and expenses — and loads everything directly into the Calculator. Once it's populated, you can immediately compare strategies with your real numbers rather than estimates.

Putting It Together

Here's a simple framework for choosing your starting strategy:

If your debts have widely different interest rates (e.g., a 25% credit card alongside a 7.5% auto loan), the avalanche method will save you meaningfully more than the snowball. The rate spread is doing real mathematical work.

If your debts have similar interest rates, the snowball becomes more attractive. The interest savings from targeting high-rate debt are smaller when rates are close together, so the psychological advantage of clearing accounts faster may outweigh the math.

If you carry multiple high-rate balances and you qualify for a personal loan at a significantly lower rate, consolidation is worth modeling before you commit to either approach. When you redirect the monthly savings back into the loan as extra payment, it can beat both the snowball and the avalanche — in total interest, time to payoff, and required minimum obligation.

If you have federal student loans, run the plan comparison before making any other decisions. Your repayment plan choice may matter more than any debt ordering strategy.

And regardless of which strategy you pick: model it. The difference between strategies, on your actual balances at your actual rates, is often far larger than people expect — and a tool that runs the math in real time takes the guesswork out entirely.

Open the ShouldIRefi Calculator to model your situation and compare strategies side by side.

The information in this article is for educational purposes only and does not constitute personalized financial advice. Individual results will vary based on specific balances, interest rates, income, and other financial factors.