If you're trying to pay off debt, you've probably heard of the snowball method and the avalanche method. Both strategies work. Both can help you get out of debt faster. But they take very different approaches — and depending on your situation, one might be a much better fit than the other.

Here's a plain-English breakdown of both, a look at which saves more money, and a way to see exactly what your numbers look like.

The Debt Snowball: Start Small, Build Momentum

The snowball method is simple: pay off your smallest debt first.

Here's how it works:

- Make minimum payments on all your debts

- Put any extra money toward your smallest balance

- Once that's paid off, take everything you were paying on it and add it to the next-smallest debt

- Keep going until all debts are gone

The name comes from the idea of a snowball rolling down a hill — it starts small but picks up more and more as it goes.

Why people love it: The snowball gives you quick wins. Paying off a debt entirely (even a small one) feels great and keeps you motivated. Research shows that people who use the snowball method are more likely to stick with their debt payoff plan because those early wins keep them going.

The tradeoff: Because you're not attacking the highest-interest debts first, you may pay more in total interest over time.

The Debt Avalanche: Attack the Highest Interest Rate First

The avalanche method is the mathematically optimal approach: pay off your highest-interest-rate debt first.

Here's how it works:

- Make minimum payments on all your debts

- Put any extra money toward the debt with the highest interest rate

- Once that's gone, move to the next-highest rate

- Continue until all debts are paid

Why it saves more money: By killing high-rate debt first, you stop the most expensive interest from compounding. Over time, this usually results in paying less total interest than the snowball method.

The tradeoff: If your highest-rate debt is also your largest balance, it can take a long time before you see a single debt fully paid off. That can feel discouraging if you need visible progress to stay motivated.

Which One Saves More Money?

The avalanche method wins on pure math. When your highest-rate debt is a large balance (like a credit card at 24%), attacking it first prevents a lot of interest from piling up.

That said, the real-world difference between the two methods isn't always dramatic. If your debts are similar in size and interest rate, the savings gap may only be a few hundred dollars. In cases where your highest-rate debt is also your smallest balance, the two methods are basically the same.

The bigger truth: the best method is the one you'll actually stick with. A plan you abandon doesn't save you anything.

A Quick Comparison

| Snowball | Avalanche | |

|---|---|---|

| Order of payoff | Smallest balance first | Highest interest rate first |

| Best for | Motivation and quick wins | Saving the most on interest |

| Saves more money? | Usually no | Usually yes |

| Works best if... | You need progress to stay motivated | You're disciplined and interest-focused |

Can You Use Both?

Yes. Some people start with the snowball to knock out a couple of small debts and build momentum, then switch to the avalanche once they're feeling confident. There's nothing wrong with combining approaches.

And if you're able to consolidate high-rate debt into a single lower-rate loan (through a personal loan, HELOC, or cash-out refinance), the strategy changes entirely — because now there's less total interest to fight against.

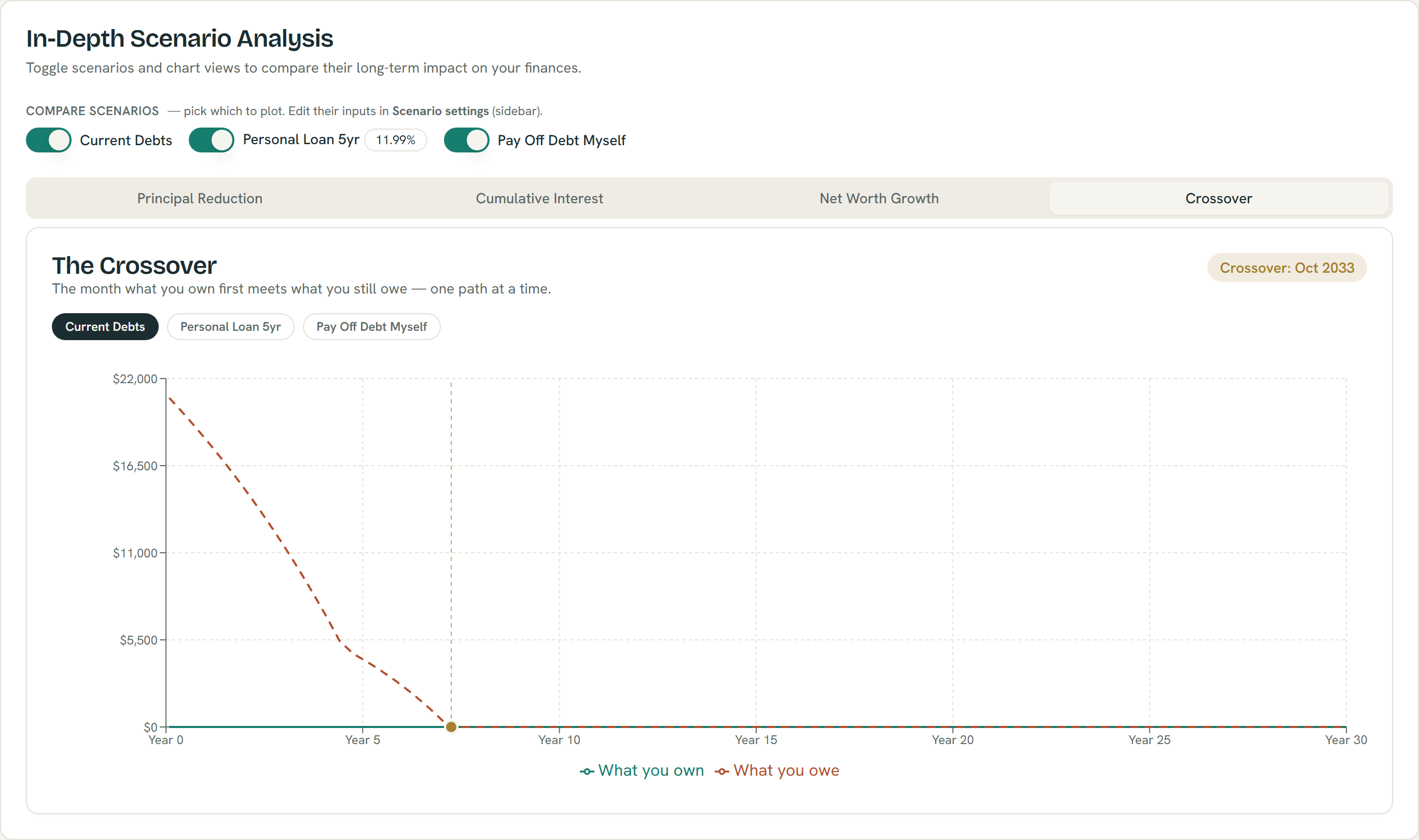

The chart marks the month your balances hit zero under the selected strategy — example data; estimates only.

Model Your Own Payoff Plan

Reading about these strategies is helpful — but seeing your own numbers makes it real.

Try the ShouldIRefi Calculator → (https://shouldirefi.app/tool/calculator)

The self-pay scenario lets you model accelerated debt paydown with extra payments. You can test different monthly amounts and see how many months earlier you'd be debt-free — and how much interest you'd save along the way.

If you're a renter without home equity, this is especially valuable — you can compare the personal loan option against a self-pay snowball or avalanche strategy and see which approach saves you more.

Not sure where to start? Take the Financial Audit (https://shouldirefi.app/tool/audit) to map your full financial picture first.