Every business acquisition loan comes down to one fraction:

DSCR = cash flow available for debt service ÷ annual debt payments

Everything else — your credit score, your resume, the seller's story — only matters after this number clears the bar.

The numerator is stricter than you think

Lenders don't use the seller's advertised cash flow. They build CFADS (cash flow available for debt service) their own way:

- Start from net income per the tax returns

- Add back interest, taxes, depreciation/amortization, and the owner's salary

- Credit only the add-backs that documents support — inflated perks get haircut

- Subtract a living salary for you (you can't pay the loan with money you need for groceries)

- Subtract salaries for any departing family members you'll have to replace

- Subtract equipment replacement spending the loan doesn't cover

That last set of subtractions is what surprises buyers: a business with "$200K cash flow" might have $130K of lender-recognized coverage once you're paid.

The denominator counts everything that demands payment

Annual principal + interest on the SBA loan, payments on any seller note (unless it's on full standby — no payments for the life of the SBA loan), equipment leases, line-of-credit interest. If it must be paid, it's in the denominator.

The thresholds

| DSCR | What happens |

|---|---|

| Below 1.15× | SBA guideline floor — lenders decline |

| 1.15–1.25× | Marginal — some lenders, more conditions |

| 1.25–1.5× | The practical bar most lenders underwrite to |

| 1.5×+ | Strong — fast approvals, better terms |

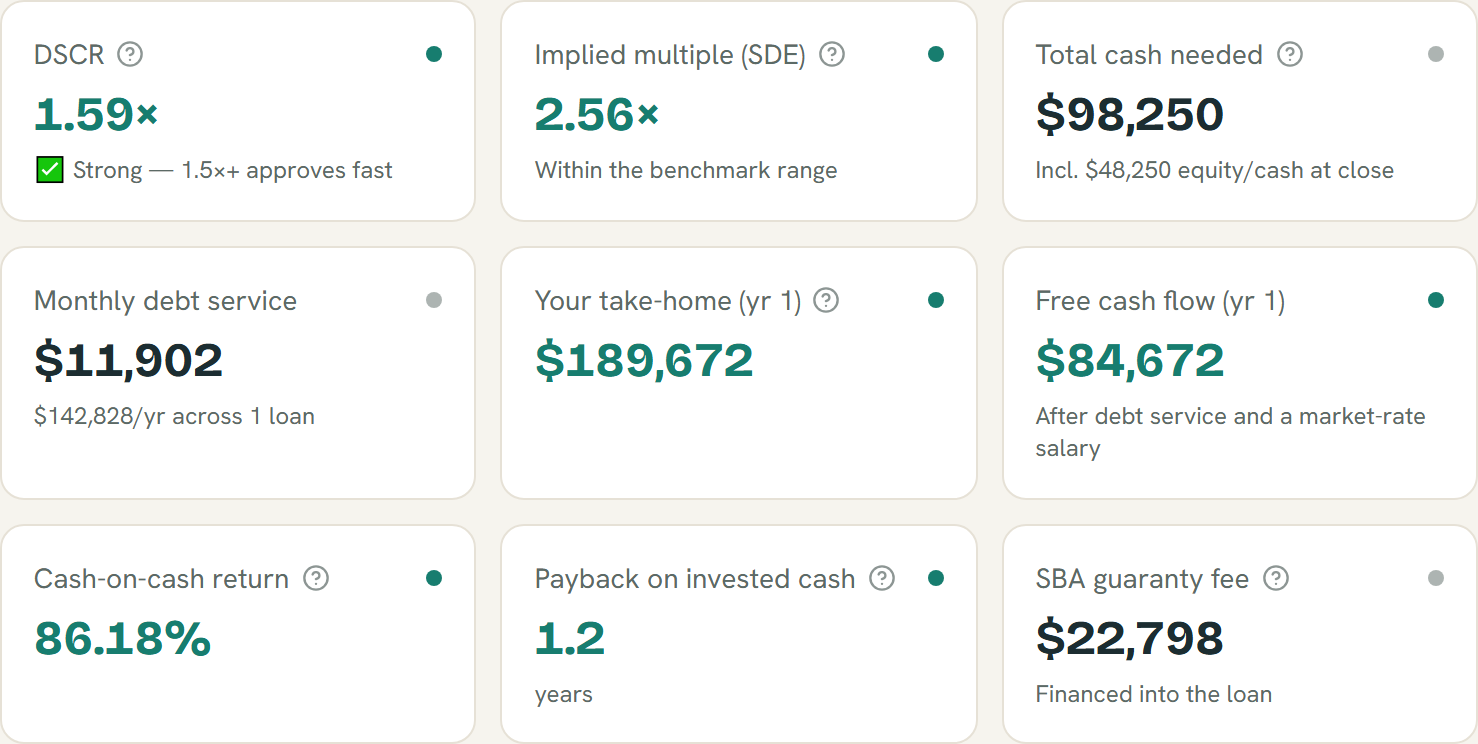

Lender-style deal metrics from example inputs — estimates built from transaction benchmarks, not an appraisal.

What to do when the number fails

DSCR failures are structural, and structure is negotiable:

- Re-trade the price — the cleanest fix; less debt, same cash flow

- Move price into a seller note on full standby — it doesn't hit the denominator

- Stretch the term — real-estate-heavy deals amortize over 25 years instead of 10

- Bring more equity — shrinks the loan directly

And remember SBA loans are variable rate: a deal that squeaks by at 1.26× today can fail after two rate bumps. Stress-test before the LOI, not after.

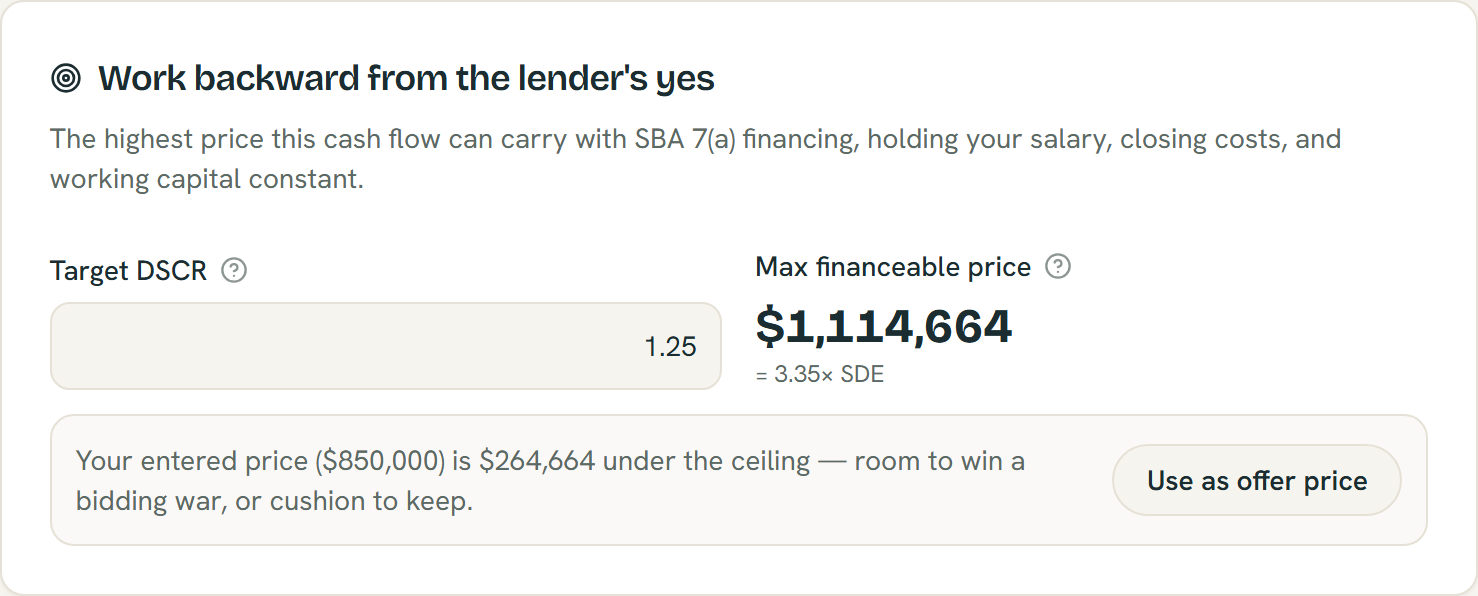

The solver works backward from the DSCR a lender needs to the highest price the cash flow can carry — example figures; estimates only.

Our free Small Business Deal Analyzer computes lender-style DSCR with a letter grade, flags failing structures with the fixes above, and includes a solver that works backward from your target DSCR to the maximum financeable price — the ceiling to carry into a negotiation.