If you have federal student loans, you have options — a lot of them. There are nine repayment plans available, and the difference between them can be hundreds of dollars per month and tens of thousands of dollars over the life of your loan.

The problem is they're confusing. Government websites are full of terms like "discretionary income," "IDR," and "AGI" that most people haven't been taught.

This guide breaks down all nine plans in plain English. No jargon, no fluff — just what you need to know.

The Two Categories: Fixed vs. Income-Driven

All federal repayment plans fall into one of two buckets:

Fixed-payment plans — Your monthly payment is based on your loan balance and interest rate. Your income doesn't factor in. These plans typically cost the least in total interest but have higher monthly payments.

Income-driven repayment (IDR) plans — Your monthly payment is based on your income and family size. These plans have lower monthly payments but stretch out the loan term (often 20–30 years), meaning you pay more interest over time — unless part of your balance is forgiven at the end.

Fixed-Payment Plans

1. Standard (10-Year) The default plan for all federal borrowers. Fixed payments over 10 years. Minimum monthly payment of $50.

- Highest monthly payment of any plan

- Lowest total interest paid

- No forgiveness

- Best for: Borrowers who can afford the payment and want to pay off loans as cheaply as possible

2. Tiered Standard (new as of July 1, 2026) Fixed payments, but the term varies based on your loan balance — from 10 to 25 years. Borrowers with larger balances get longer terms and lower monthly payments.

- No forgiveness

- Best for: New borrowers with larger balances who need a longer term without income-based payments

3. Graduated Payments start low (at roughly the interest amount) and increase every two years, with full payoff in 10 years.

- Monthly payment rises over time — works for people who expect their income to grow

- No forgiveness

- Best for: Recent graduates in career fields where income is expected to increase steadily

4. Extended (25-Year) Like standard repayment but spread over 25 years. Requires a balance of $30,000 or more.

- Lower monthly payment, much more total interest

- No forgiveness

- Best for: Borrowers with large balances who need a lower monthly payment and don't qualify for IDR

Income-Driven Repayment (IDR) Plans

All IDR plans use your Adjusted Gross Income (AGI) and family size to set your payment. Lower income and larger families = lower payment. After a set number of years of qualifying payments, any remaining balance is forgiven.

Note on current availability: PAYE and ICR stopped accepting new borrowers July 1, 2026, and are being phased out by 2028. Existing borrowers on those plans are not affected until that date.

5. IBR (New) — Income-Based Repayment for newer borrowers Payment: 10% of discretionary income Term: 20 years Forgiveness: Remaining balance forgiven after 20 years

6. IBR (Old) — Income-Based Repayment for older borrowers Payment: 15% of discretionary income Term: 25 years Forgiveness: Remaining balance forgiven after 25 years

IBR is determined by when you borrowed, not when you apply. If your loans were disbursed before July 1, 2014, you're on the older version.

7. PAYE — Pay As You Earn (closing to new borrowers July 2026) Payment: 10% of discretionary income Term: 20 years Forgiveness: After 20 years Warning: Can lead to negative amortization — if your payment is less than the monthly interest, your balance can grow over time.

8. ICR — Income-Contingent Repayment (closing to new borrowers July 2026) Payment: 20% of discretionary income, or fixed payment over 12 years — whichever is less Term: 25 years Forgiveness: After 25 years Warning: Also subject to negative amortization on some balances.

9. RAP — Repayment Assistance Plan (new as of July 1, 2026) Payment: Based on your AGI, with a step structure as income grows. Unpaid interest each month is waived — meaning your balance cannot grow. Term: 30 years Forgiveness: After 30 years Special: Payments below $50 are matched dollar-for-dollar by the government and applied to principal. Best for: Borrowers with lower or unpredictable income who want to avoid balance growth

What Is "Discretionary Income"?

All IDR plans use "discretionary income" to set your payment. It's calculated as:

AGI − (1.5 × Federal Poverty Line for your family size)

The idea is that after covering basic needs, a portion of what remains goes to your student loans. The lower your income or the larger your family, the lower the payment.

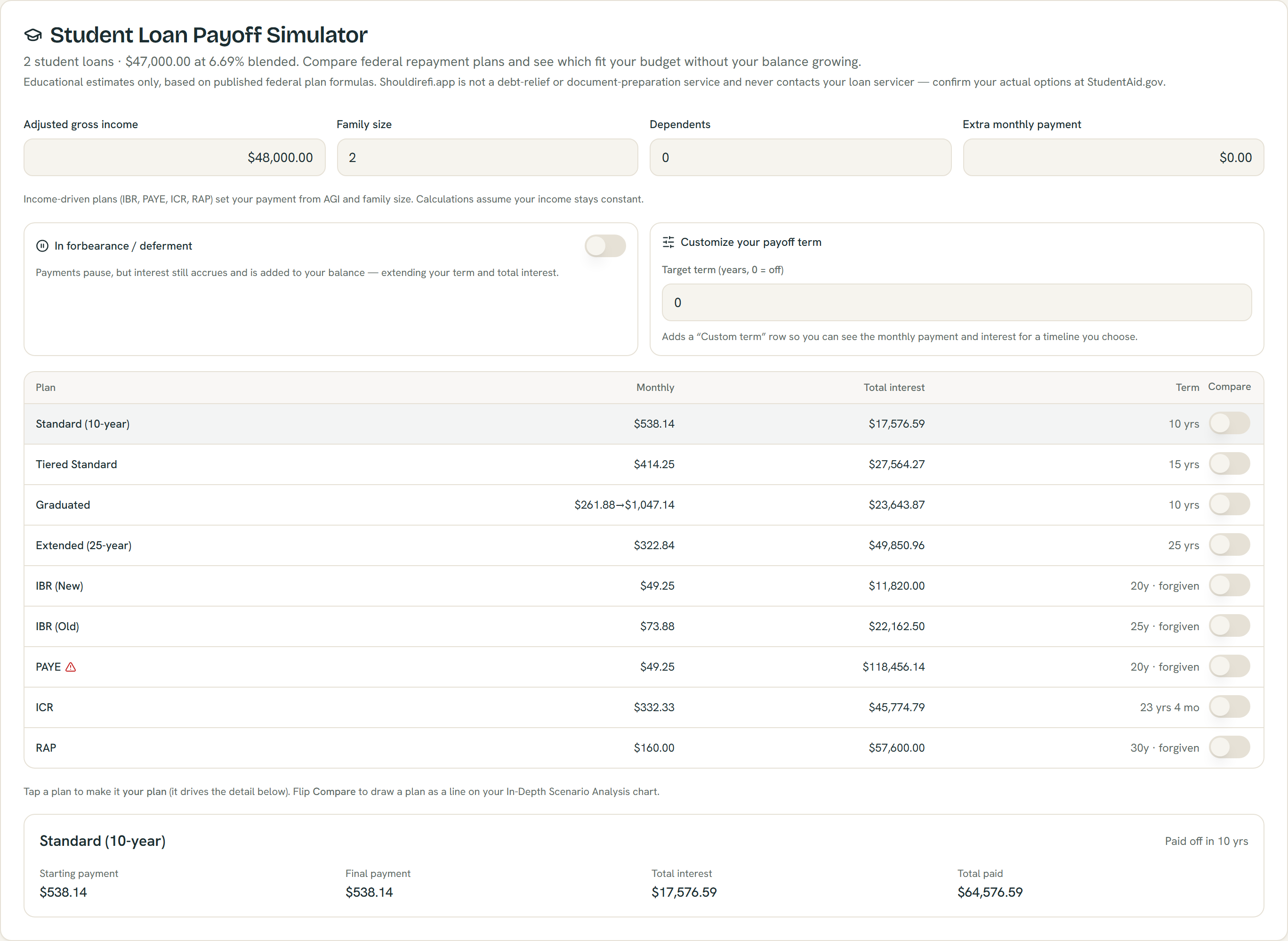

Every federal plan computed at once from example loans, with plans that can grow your balance flagged — educational estimates; confirm your options at StudentAid.gov.

How to Compare All Plans at Once

Reading this helps, but seeing your own numbers is what matters.

Try the ShouldIRefi Student Loan Simulator → (https://shouldirefi.app/tool/calculator)

The Student Loan Simulator is built into the main calculator. Enter your student loan balances (mark them as student loans), your AGI, and your family size — and the app calculates all nine repayment plans simultaneously. You can see monthly payment, total interest, loan term, and forgiveness amount for each plan, side by side.

You can also add forbearance months, test extra monthly payments, and compare your best federal plan against a personal loan payoff or refinance option — all on the same screen.

See your plan comparison → (https://shouldirefi.app/tool/calculator)