Until mid-2025 you could buy a business with essentially nothing down: a seller note could cover the entire SBA equity requirement. SOP 50 10 8 (effective June 1, 2025) ended that. The modern playbook still gets you into a deal for 5% of your own cash — but the structure has to be exactly right.

The capital stack, post-2025

For a business acquisition, the SBA requires an equity injection of 10% of total project cost — and project cost means price plus closing costs plus working capital, not just the price.

- At least 5% must be your own cash — seasoned, documented, and non-borrowed. HELOC draws and personal loans don't count for the injection.

- Up to half the injection can be a seller note on full standby: no principal or interest payments for the entire life of the SBA loan (typically 10 years).

So the classic structure on, say, a $480K project: $24K of your cash (5%) + a $24K full-standby seller note (5%) + a ~$432K SBA 7(a) loan for the rest, at Prime + up to 2.75%, amortized over 10 years (25 if real estate is most of the value), plus a financed guaranty fee.

The compliance traps

These are the mistakes that get term sheets pulled:

- A seller note with regular payments counted as equity. Only full standby counts — if the seller collects payments, the note belongs in your debt service, not your injection.

- Standby note above half the injection. 5% cash + 5% standby is the floor structure; 2% cash + 8% standby is non-compliant.

- Borrowed "cash." Lenders trace the injection. Home equity can't fund it — though it can legally fund working capital and reserves, which is often the smarter use of it anyway.

- Price above appraisal. The lender orders an independent appraisal and won't lend past it; a price above the industry multiple range is an appraisal gap waiting to happen.

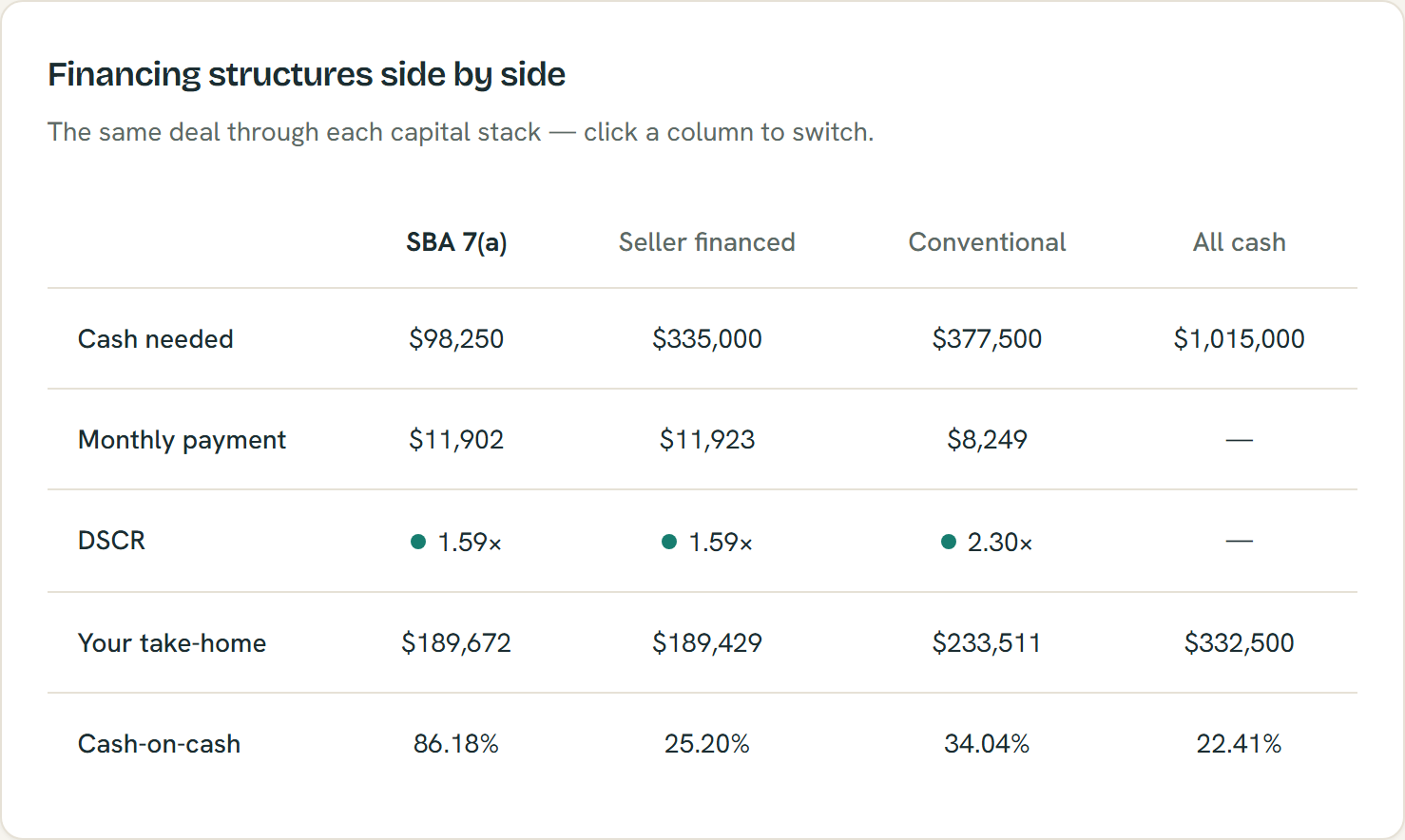

The same deal through each capital stack — example figures; estimates only.

What 5% down really costs

Down payment ≠ cash need. Add closing costs (financeable but real), working capital, and the post-close reserve you'd be reckless not to keep, and a "5% down" deal on a $2M project still wants $200K–$300K of total liquidity. Model the whole number before you fall in love with the deal.

Our free Small Business Deal Analyzer has the post-2025 rules built in as hard validation — enter a structure with 3% buyer cash or an oversized standby note and it flags the deal as non-financeable with the exact rule you broke, alongside DSCR grading and the true total-cash-needed figure. Rules are shown with their as-of date, because SOPs change.