Most first-time business buyers evaluate a deal the way the seller's broker hopes they will: look at the asking price, look at the "cash flow" line in the listing, and gut-check it. Lenders don't work that way — and neither should you. Here's the ten-minute version of a lender-grade analysis, using our free Small Business Deal Analyzer.

Step 1: Rebuild the earnings from the tax returns

Listings advertise the seller's claimed cash flow. Banks finance what the tax returns can prove. Enter net income per the returns, then add back the items that only exist because the current owner runs the business their way: the owner's salary, depreciation and amortization, interest, business taxes — and, more cautiously, owner perks and "one-time" expenses.

That last category is where deals die. If the returns show $180K of net income but the seller claims $280K of "owner benefit," a lender will discount the gap — so the analyzer has a confidence slider that credits only part of the perks and one-time claims. Watch the difference between claimed SDE and verified SDE: that spread is your negotiation ammunition.

Step 2: Check the price against real transaction data

Small businesses trade on multiples of earnings — the all-industry median has hovered around 2.6–2.7× SDE (BizBuySell transaction data), with services, manufacturing, and premium categories each having their own range. The analyzer shows where your price sits inside your industry's range, adjusted for the risk factors buyers actually price: customer concentration, a short lease, owner dependence, and recurring revenue.

Above the range isn't just "expensive" — it's a financing problem. SBA lenders order an independent appraisal and won't lend past it.

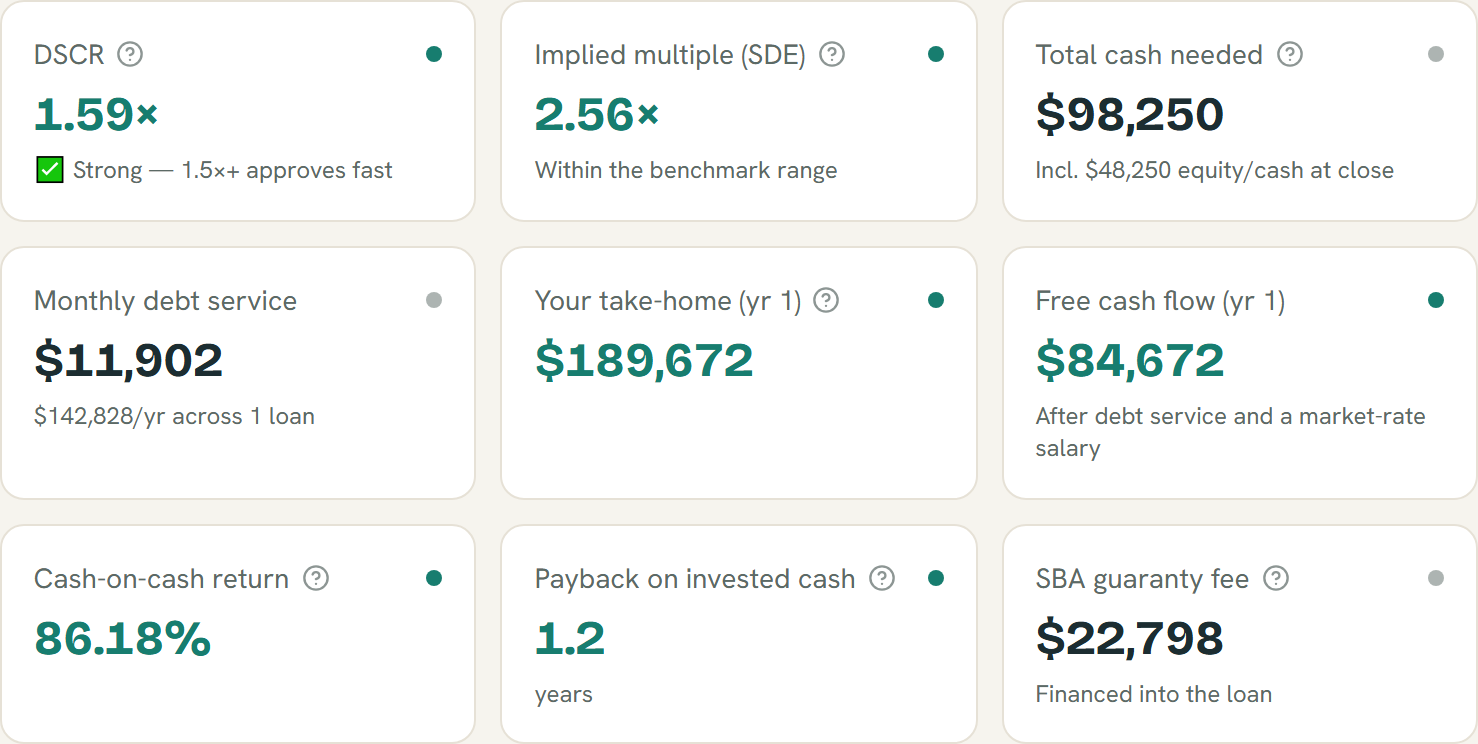

Step 3: Let DSCR gate the deal

The Debt Service Coverage Ratio — verified cash flow after your salary, divided by annual loan payments — is the number underwriting actually decides on. Below 1.15× lenders decline; most want 1.25×+; 1.5×+ approves fast. The analyzer grades this for you and, when the deal falls short, tells you the fixes that work: re-trade the price, shift some of it into a seller note, or bring more equity.

Lender-style deal metrics from example inputs — estimates built from transaction benchmarks, not an appraisal.

Step 4: Find the real cash need

"10% down" is the most misleading phrase in business buying. Between the equity injection, closing costs, working capital, and post-close reserves, a $2M acquisition typically needs $200K–$300K of total cash. The analyzer's total cash needed figure is designed to kill that surprise before you sign anything.

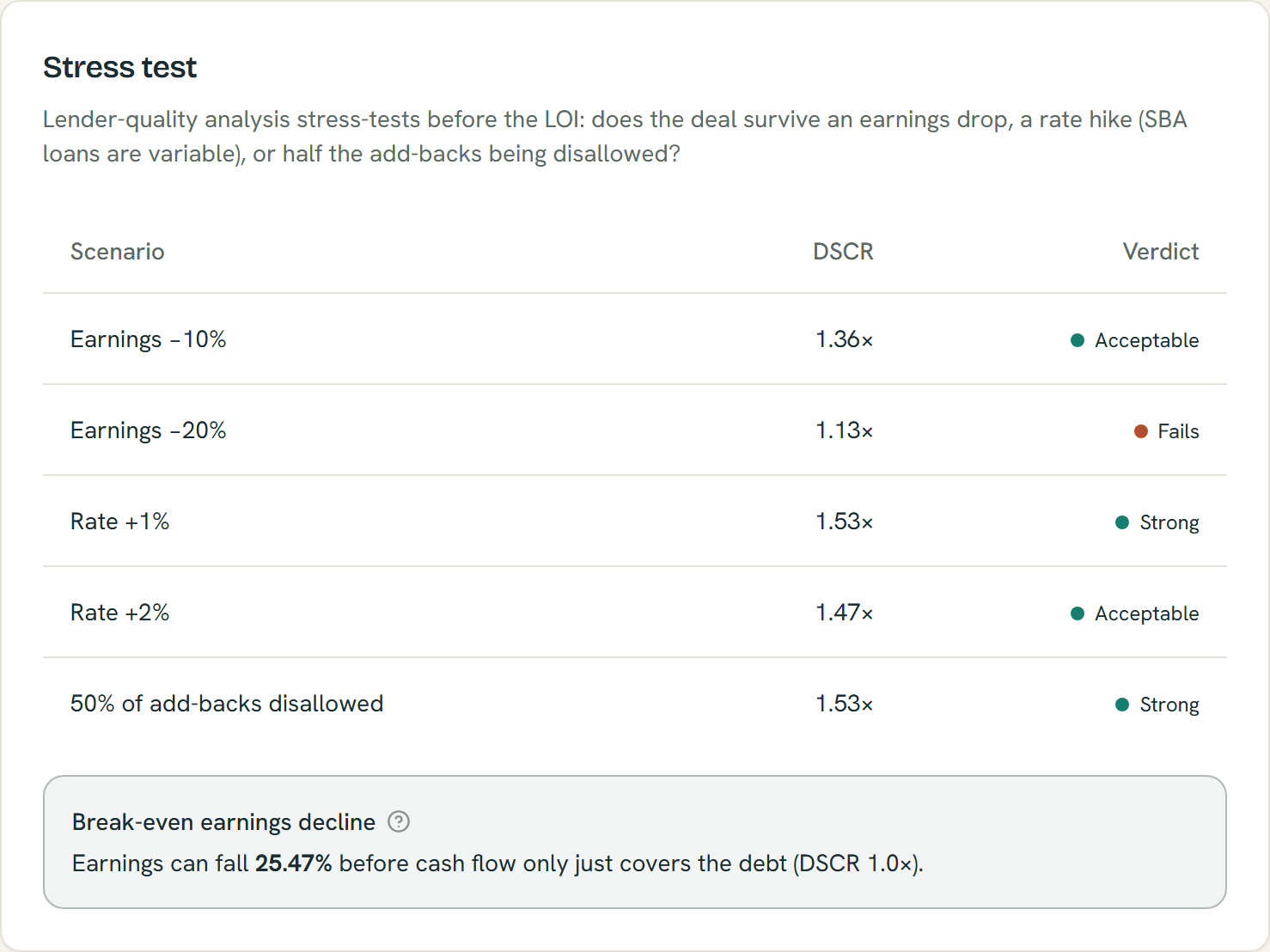

Step 5: Stress it before the LOI

Run the built-in stress tests: earnings down 10–20%, rates up 1–2 points (SBA loans float), half the add-backs disallowed. The single most useful number is the break-even earnings decline — how far the business can fall before cash flow only just covers the debt. Under 15% of cushion is thin.

Stress tests show whether the deal survives an earnings drop or a rate hike before you sign the LOI — example data; estimates only.

Ten minutes, five checks — and you'll know more about the deal than most buyers know at closing. Open the Deal Analyzer and run your numbers. (Everything it shows is an estimate from transaction benchmarks, not an appraisal — but it's the same math your lender will run.)