Your debt-to-income ratio (DTI) is one of the most important numbers in your financial life — and one of the least talked about. It affects whether you can get a loan, what interest rate you'll pay, and how much financial breathing room you actually have each month.

The good news: it's easy to calculate, and there are clear ways to improve it.

What Is DTI?

DTI is simply a percentage. It compares your total monthly debt payments to your gross monthly income (income before taxes).

The formula:

DTI = Total Monthly Debt Payments ÷ Gross Monthly Income × 100

Example:

- Monthly debt payments: credit card minimum ($100) + car loan ($350) + student loan ($200) = $650

- Gross monthly income: $4,000

- DTI = $650 ÷ $4,000 × 100 = 16.25%

That means about 16 cents of every dollar you earn goes toward debt. The rest is available for living expenses, saving, or future borrowing.

What Counts as "Debt" in This Calculation?

Include:

- Mortgage or rent payment

- Car loans

- Student loans

- Credit card minimum monthly payments

- Personal loans

- Child support or alimony

Do NOT include:

- Groceries

- Utilities (gas, electric, internet)

- Phone bills

- Insurance premiums

- Retirement contributions

Only actual debt payments count — not general living expenses.

What Does Your DTI Mean?

| DTI | What It Signals |

|---|---|

| Under 36% | Strong — most lenders see you as a good risk |

| 36–43% | Acceptable for most loans, though some may want it lower |

| 43–50% | Getting risky — harder to qualify, fewer options |

| Over 50% | Concerning — most conventional lenders will struggle to approve you |

A widely cited guideline is the 28/36 rule: your housing costs alone shouldn't exceed 28% of your income, and all debts combined shouldn't exceed 36%. This is a guideline, not a hard rule — lenders can go higher with strong credit or compensating factors.

Why Do Lenders Use It?

DTI tells a lender whether you have enough room in your budget to take on a new monthly payment. If most of your income is already going to debt, adding a new loan makes you a higher risk of falling behind.

One key point: DTI doesn't appear on your credit report. But lenders will ask about your income and calculate it when you apply for a mortgage, refinance, personal loan, or other significant credit.

What If Your DTI Is Too High?

There are four main ways to lower your DTI:

1. Pay down debt Eliminating even one debt — like a car loan or credit card balance — can meaningfully drop your monthly obligations and reduce your DTI.

2. Increase your income A raise, a side income, rental income, or a bonus that boosts your gross monthly income lowers your DTI without changing your debt at all.

3. Consolidate debt at a lower rate If you replace several higher-payment debts with a single lower-payment loan, your monthly debt total goes down — and so does your DTI.

4. Avoid taking on new debt Before applying for a mortgage or refinance, hold off on new car loans, new credit cards, or other borrowing. Each new payment raises your DTI.

DTI and Your Debt Payoff Plan

Even if you're not applying for anything right now, tracking your DTI is a useful measure of financial health. A lower DTI means more flexibility — more money left over each month after debt payments, which you can direct toward saving, investing, or paying off debt even faster.

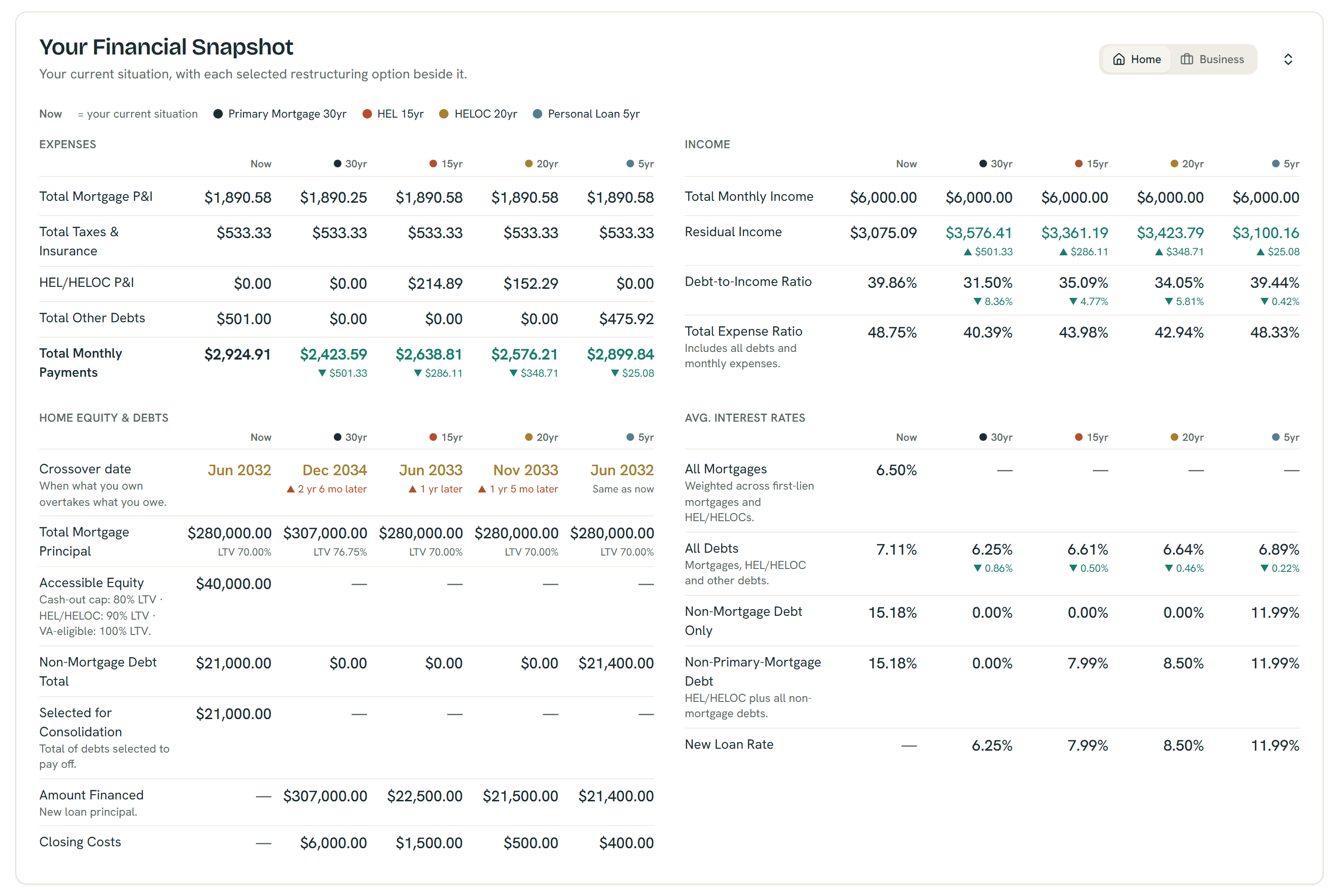

The Financial Snapshot puts every option beside your current numbers — example figures shown; all outputs are estimates, not quotes or offers.

See Your DTI — Before and After

Try the ShouldIRefi Calculator → (https://shouldirefi.app/tool/calculator)

The calculator shows your current DTI — and projects what it would look like under different scenarios. Model a personal loan, a cash-out refinance, or a self-pay strategy, and the app updates your DTI in real time. You can see exactly which approach brings your DTI into a healthier range.

It works for both homeowners (who can factor in mortgage and home equity products) and renters (who can model personal loan and self-pay options).

Try it free → (https://shouldirefi.app/tool/calculator)

Or start with the Financial Audit (https://shouldirefi.app/tool/audit) for a step-by-step walkthrough that loads your full financial picture automatically.