A lot of homeowners hear that rates have dropped and immediately think: "Should I refinance?" It's a good instinct. But refinancing isn't free, and it doesn't always save money — even when the new rate is lower.

Before you fill out a single form, here's how to figure out if refinancing is actually worth it for your situation.

Start With One Simple Question

Will the monthly savings outweigh the cost of refinancing — before you move or sell?

Refinancing costs money upfront (usually 2–5% of your loan amount in closing costs). To come out ahead, you have to stay in your home long enough for the monthly savings to pay back that cost. If you'll move before that happens, refinancing could actually cost you money.

This is called the break-even point — and it's the most important number in any refinance decision.

Three Signs Refinancing Might Work in Your Favor

1. Current rates are meaningfully lower than your rate

The bigger the gap between your current interest rate and today's rates, the more you save each month — and the faster you hit your break-even point. Even a drop of 0.5–1% can make a real difference, especially on larger loan balances.

2. Your credit score has improved

Lenders offer better rates to borrowers with higher credit scores. If your score has gone up since you got your original mortgage, you might qualify for a much better rate today — even if the market hasn't moved much.

3. Your home's value has gone up

More equity in your home means lenders see you as less risky. It may also help you drop private mortgage insurance (PMI) you've been paying, which could add significant monthly savings on top of any rate improvement.

Three Signs Refinancing Might NOT Be Worth It

1. You're planning to move soon

If you're likely to sell or move within the next couple of years, you probably won't stay in the home long enough to hit your break-even point. In that case, the closing costs you pay now may never be recovered.

2. You've already paid off a lot of your mortgage

If you're many years into a 30-year mortgage, refinancing into a new 30-year loan resets the clock. You could end up paying more total interest over time — even if your monthly payment drops.

3. The rate difference is too small for your loan balance

On a smaller loan balance, even a 1% rate drop might not save enough per month to justify closing costs. You'd have to stay in the home a very long time to break even.

How to Run Your Own Numbers

Here's the basic math to check before you refinance:

- Estimate your closing costs — typically 2–5% of your new loan amount

- Estimate your new monthly payment at the lower rate

- Subtract your new payment from your current payment = monthly savings

- Divide closing costs by monthly savings = months to break even

Example:

- Closing costs: $7,500

- Monthly savings: $250

- Break-even: 30 months (2.5 years)

If you plan to stay in the home more than 2.5 years — refinancing likely saves you money. If not, it probably doesn't.

Don't Forget: It's About More Than the Monthly Payment

Lower monthly payment ≠ better deal. Here's why:

- A longer loan term lowers your payment but can mean paying more total interest over your lifetime in the home

- A shorter term raises your payment but can save a lot in total interest and builds equity faster

- A cash-out refinance changes the math entirely — you're pulling money out, so the question becomes whether what you do with that cash saves or earns more than the cost of borrowing it

The full picture is what matters, not just the payment.

What About Paying Off Debt With a Refi?

If you're carrying high-interest debt (like credit cards at 20%+), a cash-out refinance at a much lower rate could save you a lot — even if your mortgage rate barely changes. In that case, the savings from eliminating high-interest debt can far outweigh the cost of refinancing.

This is a common reason homeowners refinance even when market rates haven't moved much in their favor.

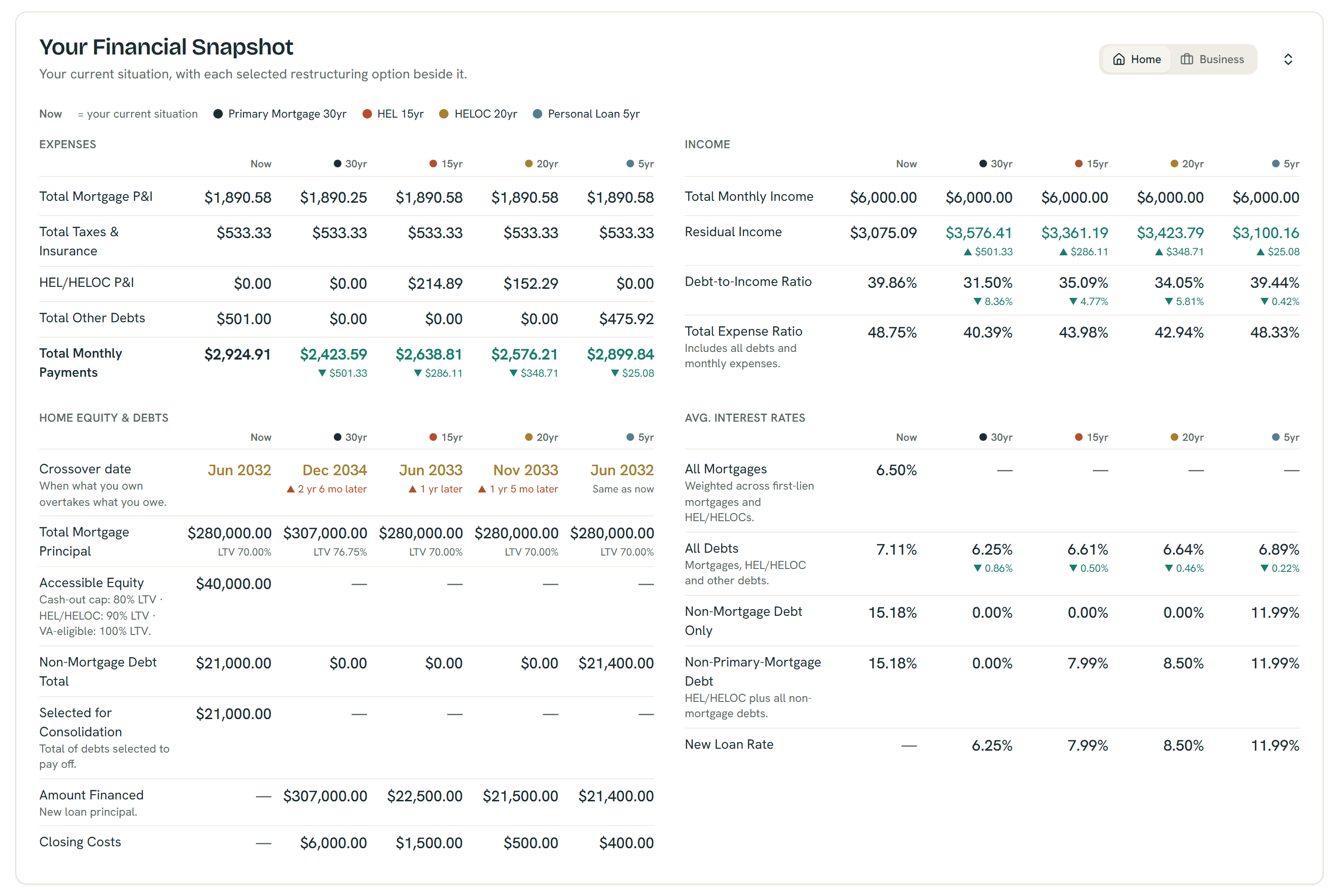

The Financial Snapshot puts every option beside your current numbers — example figures shown; all outputs are estimates, not quotes or offers.

See If It Works for Your Situation

Every homeowner's situation is different. The same rate drop that's a slam-dunk for one person might barely move the needle for another.

The fastest way to know for sure? Run your numbers in the ShouldIRefi Calculator (https://shouldirefi.app/tool/calculator).

Enter your current mortgage details, a potential new rate, and your estimated closing costs. The calculator shows you:

- Your monthly savings

- Total interest paid over the life of the loan

- Exactly how many months until you break even

- 30-year equity growth under each scenario

You can model multiple approaches side by side — rate-and-term refinance, cash-out refi, HELOC, home equity loan — and compare them all at once.

Try it free → (https://shouldirefi.app/tool/calculator)

Or if you'd like a guided walkthrough of your full financial picture, start with the Financial Audit (https://shouldirefi.app/tool/audit) — it loads all your data into the calculator automatically.