If you're on federal student loans and your payments feel too high for your income, income-driven repayment (IDR) plans can bring them down dramatically — sometimes to as low as $0 per month.

But there are several plans to choose from, and the differences matter. Here's a plain-English breakdown of IBR, PAYE, ICR, and the new RAP plan that launched in 2026.

Important note: The student loan repayment landscape changed significantly in 2025 and 2026. PAYE and ICR are being phased out — they closed to new borrowers on July 1, 2026, and will sunset entirely in 2028. IBR remains permanent. RAP launched July 1, 2026, as the new income-driven option.

How All IDR Plans Work

Before comparing specific plans, here's the shared foundation:

All IDR plans use your Adjusted Gross Income (AGI) and family size to calculate a discretionary income figure. Your monthly payment is then set as a percentage of that discretionary income.

Discretionary income = AGI − (1.5 × federal poverty guideline for your family size)

The lower your income or the larger your family, the lower your payment. At very low incomes, the payment can be $0.

After making qualifying payments for a set number of years, any remaining balance is forgiven — but under current law (since January 2026), that forgiven amount is treated as taxable income in the year of forgiveness.

IBR — Income-Based Repayment

IBR is the most widely available income-driven plan and the only legacy plan that is NOT being phased out. Any borrower with eligible Direct Loans or FFEL loans can now enroll (the partial financial hardship requirement was removed by the One Big Beautiful Bill Act).

There are two versions based on when you borrowed:

New IBR (first loan disbursed on or after July 1, 2014):

- Payment: 10% of discretionary income

- Term: 20 years → forgiveness of remaining balance

- Payment cap: Won't exceed what you'd pay on the Standard 10-year plan

Old IBR (first loan disbursed before July 1, 2014):

- Payment: 15% of discretionary income

- Term: 25 years → forgiveness of remaining balance

- Payment cap: Same — won't exceed Standard plan amount

Watch out for: IBR does not eliminate negative amortization. If your payment doesn't cover monthly interest, your balance can grow.

PAYE — Pay As You Earn (closing to new borrowers July 2026)

PAYE works similarly to New IBR — 10% of discretionary income, 20-year forgiveness — but has different eligibility rules and one key difference:

- Payments are capped at the 10-year Standard plan amount

- Closed to new borrowers July 1, 2026; sunsets July 1, 2028

- Borrowers already on PAYE can stay until the 2028 sunset

- Risk: Can experience negative amortization (balance growth) when payments are very low

If you're currently on PAYE and approaching the 2028 sunset, you'll need to transition to IBR or RAP.

ICR — Income-Contingent Repayment (closing to new borrowers July 2026)

ICR is the oldest income-driven plan and has broader loan eligibility than other IDR plans.

- Payment: Lower of 20% of discretionary income OR fixed payment over 12 years adjusted for income

- Term: 25 years → forgiveness

- Closed to new borrowers July 1, 2026; sunsets July 1, 2028

- Special relevance: ICR is the only IDR plan available to Parent PLUS loan borrowers (after consolidation into a Direct Consolidation Loan)

- Risk: Can also experience negative amortization

RAP — Repayment Assistance Plan (new July 2026)

RAP is the newest income-driven plan and addresses one of the biggest problems with older IDR plans: negative amortization.

- Payment: Calculated as 1–10% of AGI (based on a stepped bracket system), minimum $10/month

- Term: 30 years → forgiveness

- Key advantage: Unpaid interest is waived each month — your balance cannot grow

- Key advantage: If your payment doesn't reduce principal by $50, the government contributes up to $50/month toward principal

- Parent PLUS: NOT eligible, even after consolidation

RAP is the only plan available to new borrowers (those who take out their first loan on or after July 1, 2026). Existing borrowers can also switch to RAP.

Side-by-Side Comparison

| New IBR | Old IBR | PAYE | ICR | RAP | |

|---|---|---|---|---|---|

| Payment | 10% discretionary | 15% discretionary | 10% discretionary | 20% discr. or 12-yr fixed | 1–10% of AGI |

| Forgiveness at | 20 years | 25 years | 20 years | 25 years | 30 years |

| Negative amortization? | Possible | Possible | Possible | Possible | No (interest waived) |

| Parent PLUS eligible? | No | No | No | Yes (after consolidation) | No |

| New enrollment? | Open | Open | Closing July 2026 | Closing July 2026 | Open |

Which Plan Is Right for You?

Choose New IBR if: You borrowed after July 1, 2014, want a permanent plan, and 10% of discretionary income is manageable.

Choose Old IBR if: You borrowed before July 2014 and your payment under Old IBR is affordable (sometimes Old IBR payments are lower than newer plans depending on your situation).

Choose RAP if: Your income is low, you want to avoid balance growth (negative amortization), or you're a new borrower who doesn't have other options.

Stay on PAYE or ICR for now if: You're already enrolled and your current payment is lower than what IBR or RAP would give you — though you'll need to transition by 2028.

ICR via consolidation if: You have Parent PLUS loans and need access to an income-driven plan.

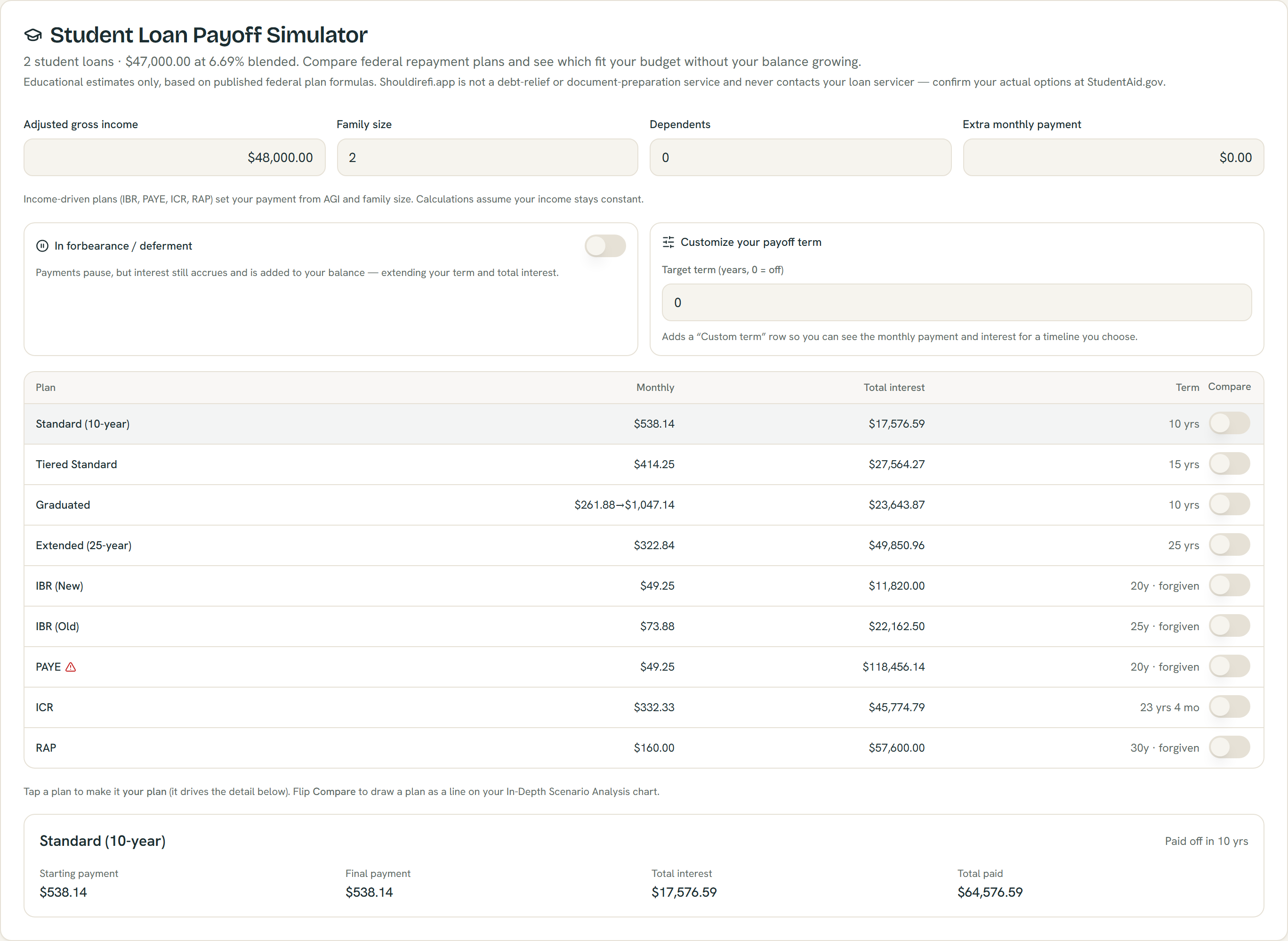

Every federal plan computed at once from example loans, with plans that can grow your balance flagged — educational estimates; confirm your options at StudentAid.gov.

Compare All Plans at Once

Try the ShouldIRefi Student Loan Simulator → (https://shouldirefi.app/tool/calculator)

Enter your loans, income, and family size, and the app calculates all plans simultaneously — including IBR, PAYE, ICR, RAP, and all fixed-payment plans. You can see exactly what your monthly payment would be, how much total interest you'd pay, and what (if any) balance would be forgiven at the end of each term.

You can also compare your best federal plan against paying off the loans faster with extra payments, or against a personal loan consolidation.

See your personalized plan comparison → (https://shouldirefi.app/tool/calculator)