Most homeowners know two ways to pay off a mortgage faster: refinance to a lower rate, or make extra payments every month.

There’s a third option most people have never heard of. It doesn’t require you to qualify for a new loan. It doesn’t involve closing costs. And it can lower your monthly payment immediately while still getting you out of debt years ahead of schedule.

It’s called a mortgage recast — and once you understand how it works, there’s a strategy built on top of it that can supercharge your payoff timeline in a way that keeps getting faster the longer you do it.

What Is a Mortgage Recast?

A recast is when you make a large lump-sum payment toward your mortgage principal, and your lender re-calculates your monthly payment based on the new, lower balance.

Your interest rate stays the same. Your loan term stays the same. But because your remaining balance is now smaller, the payment required to pay it off in the same timeframe goes down.

Here’s a simple example:

Say you have a $280,000 remaining balance on a 30-year mortgage at 7% with 22 years left. Your monthly payment is about $1,864.

Now suppose you make a $50,000 lump-sum payment toward principal. Your balance drops to $230,000. Your lender recasts the loan — re-amortizing that $230,000 over the remaining 22 years at the same 7% rate.

Your new monthly payment: about $1,530.

That’s a drop of roughly $334 per month — permanently, for the rest of the loan. And you didn’t have to refinance, pull your credit, or pay closing costs. You just made one large payment.

How Recasting Is Different From Refinancing

These two things sound similar but work very differently.

| Recast | Refinance | |

|---|---|---|

| Changes interest rate | No | Yes |

| Changes loan term | No | Yes (you pick a new one) |

| Requires new application | No | Yes |

| Credit check required | No | Yes |

| Closing costs | Minimal ($150–$500) | Typically $3,000–$6,000+ |

| Lowers monthly payment | Yes | Yes |

| Available to all borrowers | No (some loan types excluded) | Most borrowers qualify |

Recasting is simpler, cheaper, and faster than refinancing. The tradeoff: you’re not changing your rate. If your rate is already competitive, that’s fine. If rates have dropped significantly since you originated the loan, a refinance might be a better move — or you might do both at different times.

A few things to know about eligibility: most conventional loans can be recast, but FHA loans, VA loans, and USDA loans typically cannot. Jumbo loans are often eligible. You’ll need to check with your lender, as not all servicers offer recasting, and the minimum lump-sum requirement varies — typically somewhere in the range of 10% of your remaining balance, though many lenders set specific dollar thresholds.

Why Not Just Make Extra Monthly Payments?

This is the most common question. If you have extra cash each month, why not just put it directly toward the mortgage?

Extra monthly payments absolutely work. They reduce principal, cut interest, and shorten the loan. There’s nothing wrong with that approach.

But the recast strategy described below has some advantages:

1. You earn interest on your savings while you accumulate the lump sum.

If you’re setting aside money in a high-yield savings account at 4–5%, that money is working for you during the accumulation period. Extra monthly mortgage payments don’t earn anything — they’re gone the moment you make them.

2. Recasting permanently lowers your required payment.

When you make extra monthly payments, your required minimum payment stays the same. A recast actually reduces it. That lower payment gives you more flexibility — and in this strategy, you redirect it to build toward the next recast even faster.

3. The effect compounds over time.

Each recast lowers your payment. That freed-up cash goes into savings. You reach the next recast threshold sooner. Which lowers your payment further. Which accelerates the next one. The strategy builds momentum with each cycle.

The Savings-Powered Recast Strategy

Here’s the full approach, step by step.

Step 1: Set your monthly savings target.

Pick an amount you can save consistently each month — the equivalent of what you’d otherwise put toward extra mortgage payments. Put it in a high-yield savings account (HYSA) earning competitive interest rather than sending it to the mortgage servicer.

Step 2: Accumulate until you hit roughly 20% of your remaining principal.

This is your recast threshold. At this level, you’re making a meaningful dent in the balance — enough for the lender to re-amortize the loan at a noticeably lower payment. (Check with your lender for their specific minimum, which may be lower — this threshold is a planning target to ensure a meaningful payment reduction.)

Step 3: Submit the lump-sum payment and request a recast.

Contact your servicer, make the principal payment, and request the recast. Pay the small administrative fee (typically $150–$500). Your new, lower monthly payment kicks in — usually within one billing cycle.

Step 4: Increase your monthly savings rate by the full amount your payment dropped.

This is the key move. If your payment dropped by $300/month, add that $300 to what you’re saving each month. Your lifestyle doesn’t change. But your savings rate just went up by $300.

Step 5: Repeat.

Keep accumulating in the HYSA. When you reach 20% of your new, lower balance, recast again. Your payment drops again. Your savings rate goes up again. The cycle accelerates.

What This Looks Like in Practice

Here’s a simplified illustration to show the momentum effect.

Assume a $300,000 original balance at 7%, 30-year term, with $250,000 remaining and 24 years left. You’re saving $600/month in a HYSA earning 4.5%.

Round 1:

| Round 1 | |

|---|---|

| Starting balance | $250,000 |

| Recast target (20%) | ~$50,000 |

| Monthly savings | $600/month + 4.5% HYSA interest |

| Time to accumulate | ~6.5–7 years |

| New balance after recast | ~$200,000 |

| Payment drop | ~$333/month ($1,864 → $1,531) |

| New savings rate | $600 + $333 = $933/month |

Round 2:

| Round 2 | |

|---|---|

| Starting balance | $200,000 |

| Recast target (20%) | ~$40,000 |

| Monthly savings | $933/month + 4.5% HYSA interest |

| Time to accumulate | ~3.5–4 years |

| New balance after recast | ~$160,000 |

| Payment drop | ~$306/month ($1,531 → $1,225) |

| New savings rate | $933 + $306 = $1,239/month |

Round 3:

| Round 3 | |

|---|---|

| Starting balance | $160,000 |

| Recast target (20%) | ~$32,000 |

| Monthly savings | $1,239/month + 4.5% HYSA interest |

| Time to accumulate | ~2–2.5 years |

| New balance after recast | ~$128,000 |

| Payment | ~$980/month |

Notice the pattern. Round 1 took nearly 7 years. Round 2 took 4. Round 3 took less than 2.5. Each cycle is faster than the last because you’re saving more after each payment drop.

That’s the compound effect working in your favor.

The Interest Advantage

One detail that makes this strategy better than pure extra payments: your savings are earning interest during the accumulation phase.

At 4.5% in a HYSA, $600/month over 6.5 years doesn’t just add up to $46,800 — it compounds to roughly $50,000. The interest is effectively helping you reach your recast target without contributing any additional money.

This advantage shifts based on the difference between your mortgage rate and available savings rates. When savings rates are high and your mortgage rate is comparatively lower, the math strongly favors accumulating in the HYSA first. When mortgage rates are much higher than savings rates, extra monthly payments become more attractive.

[Model both strategies side by side →] https://shouldirefi.app/tool/calculator

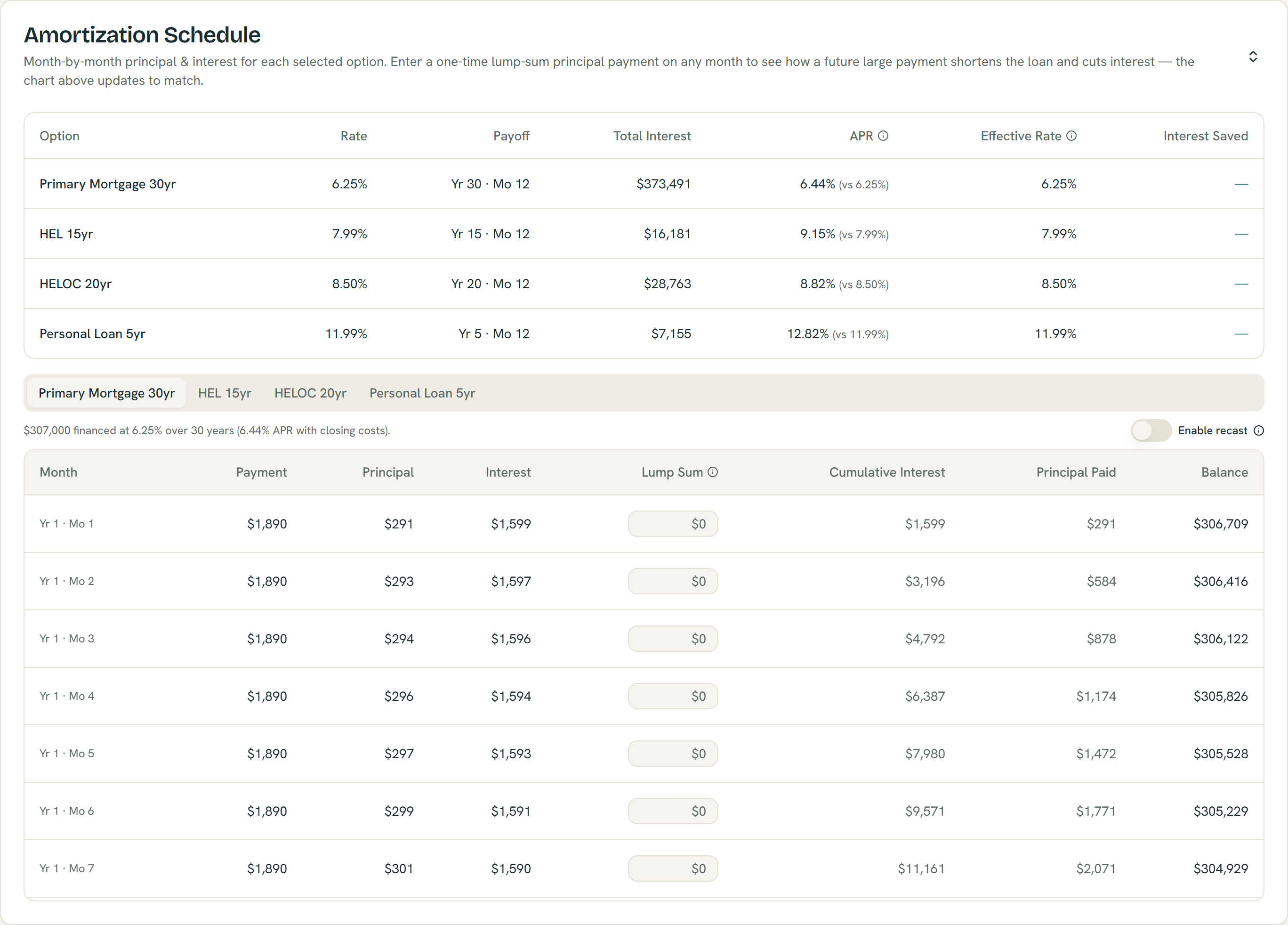

The Amortization Schedule breaks down every payment and lets you model one-time lump sums — with an optional recast — from example inputs; estimates only.

Who This Strategy Is Best For

Strong fit if:

• You have a competitive rate and don’t want to refinance

• Your loan type is eligible for recasting (conventional or jumbo — check with your servicer)

• You can maintain discipline putting money into savings rather than spending it

• You want the flexibility of a lower required payment each month

• You have a stable income and a long remaining loan term

Less ideal if:

• Your loan isn’t eligible for recasting (FHA, VA, USDA)

• Your interest rate is high enough that refinancing would save more in the long run

• You struggle with keeping savings separate from spending money

• You’re very close to paying off the loan already

A Note on Taxes and Emergency Funds

Before putting every spare dollar into this strategy, make sure your financial foundation is solid. Keep a healthy emergency fund separate from your recast savings. A fully-funded emergency reserve means you won’t have to tap your recast savings if something unexpected comes up — which would set your timeline back and potentially mean missing a recast cycle.

Also, mortgage interest is sometimes tax-deductible (depending on your situation and tax bracket). If you’re currently deducting mortgage interest, reducing your balance faster also reduces that deduction over time. This is unlikely to change whether the strategy makes sense, but it’s worth discussing with a tax professional if it’s a significant part of your tax picture.

See How Fast You Could Pay Off Your Mortgage

The best way to know if this strategy is right for you is to model your specific numbers — your current balance, rate, remaining term, how much you can save each month, and what savings rates are available to you right now.

[Try the ShouldIRefi Calculator →] https://shouldirefi.app/tool/calculator

The calculator lets you model scenarios including extra payments and lump-sum paydown, so you can compare the recast strategy against alternatives like a refinance or standard extra monthly payments — and see the total interest, payoff timeline, and monthly payment under each.

Not sure what numbers to start with? [Start with the Financial Audit] _https://shouldirefi.app/tool/audit_— it walks you through your full financial picture step by step and loads everything into the calculator automatically.