Most people assume that making payments on a loan means the balance goes down. With student loans on certain repayment plans, that's not always true. Sometimes your balance can actually grow — even when you're making payments on time, every month.

This is called negative amortization, and it affects some borrowers on income-driven repayment plans. Here's what you need to know.

What Is Negative Amortization?

Every month, your student loan charges interest on the outstanding balance. When your monthly payment is less than the interest that accrues, the unpaid interest gets added to your loan balance.

Over time, this means you could owe more than when you started — even after years of payments.

Simple example:

- Monthly interest accrual: $250

- Monthly payment (based on your income): $175

- Unpaid interest: $75 per month

After one year, that adds up to $900 added to your balance — on top of the principal you already owed. After several years at low income, the balance could be significantly higher than the original loan amount.

Which Repayment Plans Can Cause This?

Not all income-driven plans carry this risk. Here's where it can happen:

PAYE (Pay As You Earn) Monthly payments are set at 10% of discretionary income. If that payment doesn't cover your monthly interest, the shortfall is added to your balance. PAYE does limit this somewhat — unpaid interest can only be capitalized up to 10% of the original loan balance you had when you enrolled.

Note: PAYE is no longer accepting new borrowers as of July 1, 2026, and will sunset completely in 2028. Borrowers already on PAYE can remain until that date.

ICR (Income-Contingent Repayment) Payments can be set low enough to create negative amortization, and unpaid interest is added to the principal annually. ICR is also closing to new borrowers July 1, 2026, with full sunset in 2028.

IBR (Income-Based Repayment) IBR doesn't eliminate negative amortization entirely, but it does limit it. If your payment doesn't cover interest, there's some protection against interest capitalization under IBR.

Which Plans Prevent Negative Amortization?

RAP (Repayment Assistance Plan) — launched July 1, 2026 RAP was specifically designed to eliminate negative amortization. If your monthly payment doesn't cover the interest that accrued, the remaining interest is waived — not added to your balance. Your loan balance cannot grow under RAP, even at the lowest payment amounts. This is one of RAP's biggest advantages over older income-driven plans.

Additionally, if your payment doesn't reduce your principal by at least $50, the federal government chips in up to $50 per month toward principal — ensuring your balance actually decreases each month.

Why Does It Matter?

If you're planning to reach forgiveness at the end of your repayment term, negative amortization can dramatically increase the amount forgiven — which may also mean a larger tax bill. IDR forgiveness (for plans other than PSLF) is treated as taxable income under current law, so a bigger forgiven balance could mean a bigger tax bill in the year of forgiveness.

If you're trying to pay off your loans entirely rather than rely on forgiveness, negative amortization works against you — you may be making payments for years while your balance grows.

How to Know If This Is Happening to You

The clearest sign: log in to your loan servicer account and track your balance month over month. If it's growing despite on-time payments, you're experiencing negative amortization.

You can also check by comparing your monthly payment to your monthly interest charge, which your servicer should be able to tell you.

Should You Switch Plans?

If you're on PAYE or ICR and experiencing negative amortization — and you're not pursuing forgiveness — it may be worth switching to IBR or RAP, which offer better protection against balance growth.

If you are pursuing forgiveness, the math is more complex. A lower payment now (even if it causes the balance to grow) may still result in more total forgiveness at the end of the term. But that larger forgiven balance also creates a larger potential tax liability — the "tax bomb."

The right answer depends heavily on your specific loan amounts, income, family size, and long-term plans.

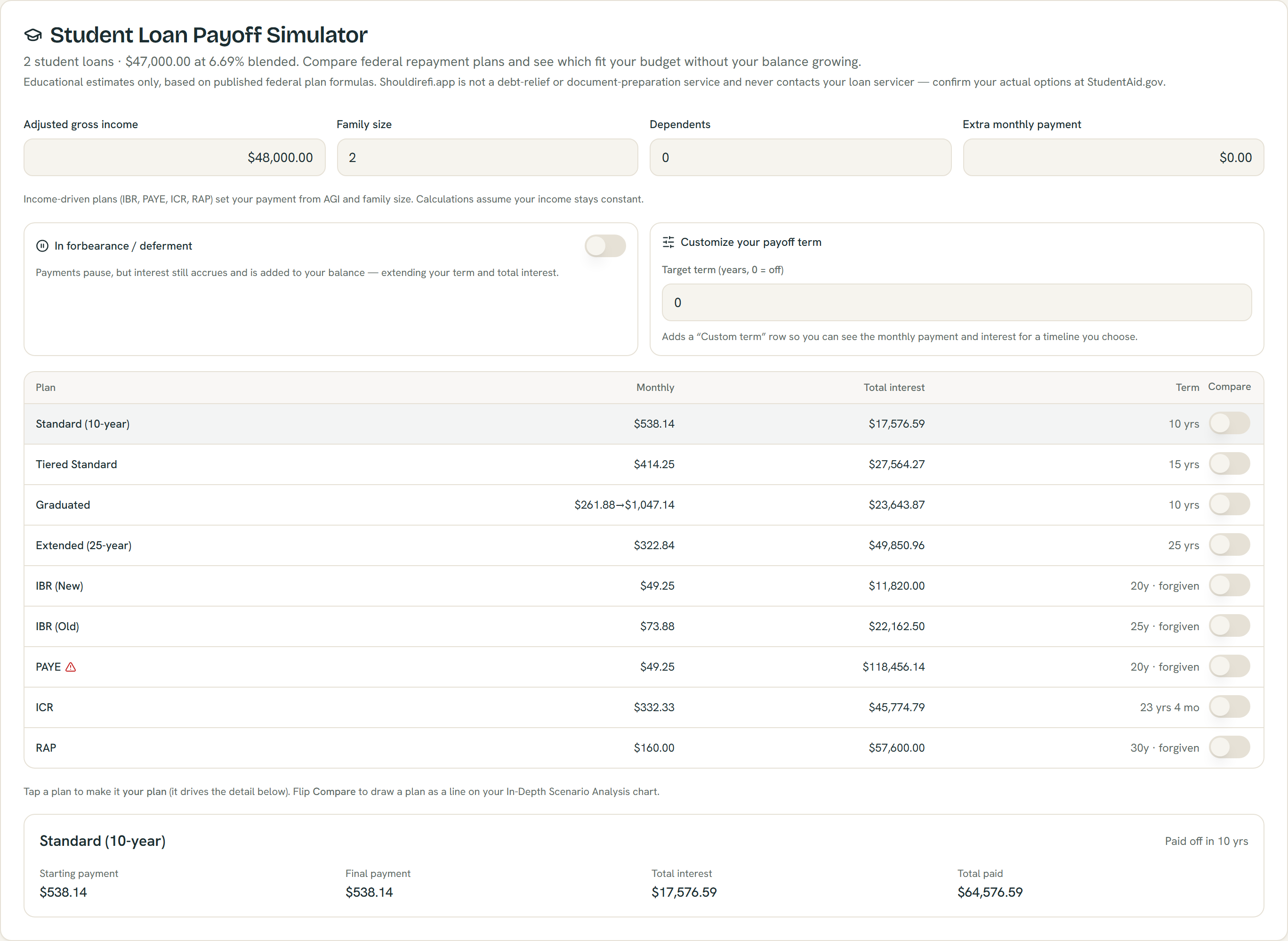

Every federal plan computed at once from example loans, with plans that can grow your balance flagged — educational estimates; confirm your options at StudentAid.gov.

See How Each Plan Affects Your Balance

Try the ShouldIRefi Student Loan Simulator → (https://shouldirefi.app/tool/calculator)

When you enter your student loans and income, the simulator calculates all repayment plans simultaneously — including which ones could cause negative amortization. The app flags plans where your balance would grow, shows the peak balance and forgiven amount, and recommends switching to RAP (which eliminates this risk).

You can also add extra payments to any plan and see how that changes the picture.

See your plan comparison → (https://shouldirefi.app/tool/calculator)