If you took out Parent PLUS loans to help pay for your child's college education, you may have discovered that the repayment options are surprisingly limited compared to regular student loans.

The situation got even more complicated in 2026, when major changes to the federal student loan system took effect. Here's a clear breakdown of what you're working with.

What Are Parent PLUS Loans?

Parent PLUS loans are federal loans that parents borrow — not the student — to cover the cost of a child's undergraduate education. The parent is solely responsible for repayment.

Unlike regular student loans, Parent PLUS loans have historically had very limited access to income-driven repayment plans. And those limitations just got tighter.

What Repayment Plans Are Available?

Standard repayment plans are available to all Parent PLUS borrowers:

- Standard Plan — Fixed payments over 10 years (or 10–25 years for the Tiered Standard Plan, which launched July 2026). This is the default if you don't choose something else.

- Graduated Plan — Payments start low and increase every two years, paid off in 10 years.

- Extended Plan — For large balances, payments spread over 25 years.

These plans don't adjust for income. If your income drops, your payment doesn't.

Can Parent PLUS Loans Use Income-Driven Repayment?

This is where it gets complicated.

Parent PLUS loans do NOT automatically qualify for income-driven repayment (IDR). They cannot directly enroll in IBR, PAYE, or the new RAP plan.

However, there is a path:

You can consolidate Parent PLUS loans into a Direct Consolidation Loan and then enroll in the ICR (Income-Contingent Repayment) plan.

After making one payment on ICR, you may then be eligible to switch to IBR.

Critical Deadline: The July 2026 Cutoff

Under changes that took effect in 2026, this consolidation pathway is now time-limited.

Parent PLUS loans borrowed before July 1, 2026: You can still consolidate into a Direct Consolidation Loan and access ICR — but only if the consolidation was completed before the July 1, 2026 deadline. (Applications needed to be submitted around April 1, 2026, due to 4–6 week processing times.)

Parent PLUS loans borrowed on or after July 1, 2026: These loans can only be repaid on the Standard Plan. They are permanently ineligible for any income-driven plan — including the new RAP plan — even if consolidated.

Additionally, taking out a new Parent PLUS loan on or after July 1, 2026 can affect your existing loans: if you had previously consolidated older Parent PLUS loans and enrolled in ICR, borrowing a new post-July 2026 Parent PLUS loan may cause all your Parent PLUS loans to lose IDR eligibility.

ICR: The Only IDR Option (For Now)

ICR (Income-Contingent Repayment) calculates your payment as the lesser of:

- 20% of your discretionary income, or

- What you'd pay on a fixed 12-year plan adjusted for your income

ICR is being phased out by July 2028, but borrowers already enrolled can stay on it. When ICR ends, those borrowers are expected to transition to IBR (if eligible) automatically.

After making one qualifying payment on ICR, Parent PLUS borrowers who consolidated before the July 2026 deadline may be able to switch to IBR — which generally offers lower payments than ICR for most borrowers.

Can Parent PLUS Loans Be Forgiven?

There are two forgiveness paths, both requiring prior consolidation into a Direct Consolidation Loan:

ICR Forgiveness — after 25 years Remaining balance is forgiven after 300 qualifying payments. Under current law (since January 2026), forgiven amounts are treated as taxable income.

PSLF — after 10 years If you work full-time for a qualifying government or nonprofit employer, remaining balance is forgiven tax-free after 120 qualifying payments. Parent PLUS loans that were consolidated and enrolled in IDR before the July 2026 deadline may be eligible for PSLF.

New Parent PLUS loans (borrowed after July 2026) on the Standard Plan can technically count toward PSLF — but in practice, there may be no remaining balance to forgive after 10 years of fixed standard payments.

New Borrowing Limits (Starting July 2026)

For parents borrowing new Parent PLUS loans after July 1, 2026:

- $20,000 annual cap per student

- $65,000 lifetime cap per student

Previous Parent PLUS loans had no hard limit — parents could borrow up to the full cost of attendance. These new caps are significant, especially for borrowers at high-cost institutions.

What Should Parent PLUS Borrowers Do?

If you have existing Parent PLUS loans:

- Check whether you consolidated before July 1, 2026

- If consolidated, confirm you're enrolled in ICR or an eligible IDR plan

- If not yet consolidated and the deadline has passed, you are limited to standard repayment plans

If you're planning to borrow new Parent PLUS loans:

- Understand that new loans after July 2026 are locked into the Standard Plan with no IDR options

- Factor in the new annual and lifetime caps

- Consider whether the borrowing limit affects your plans

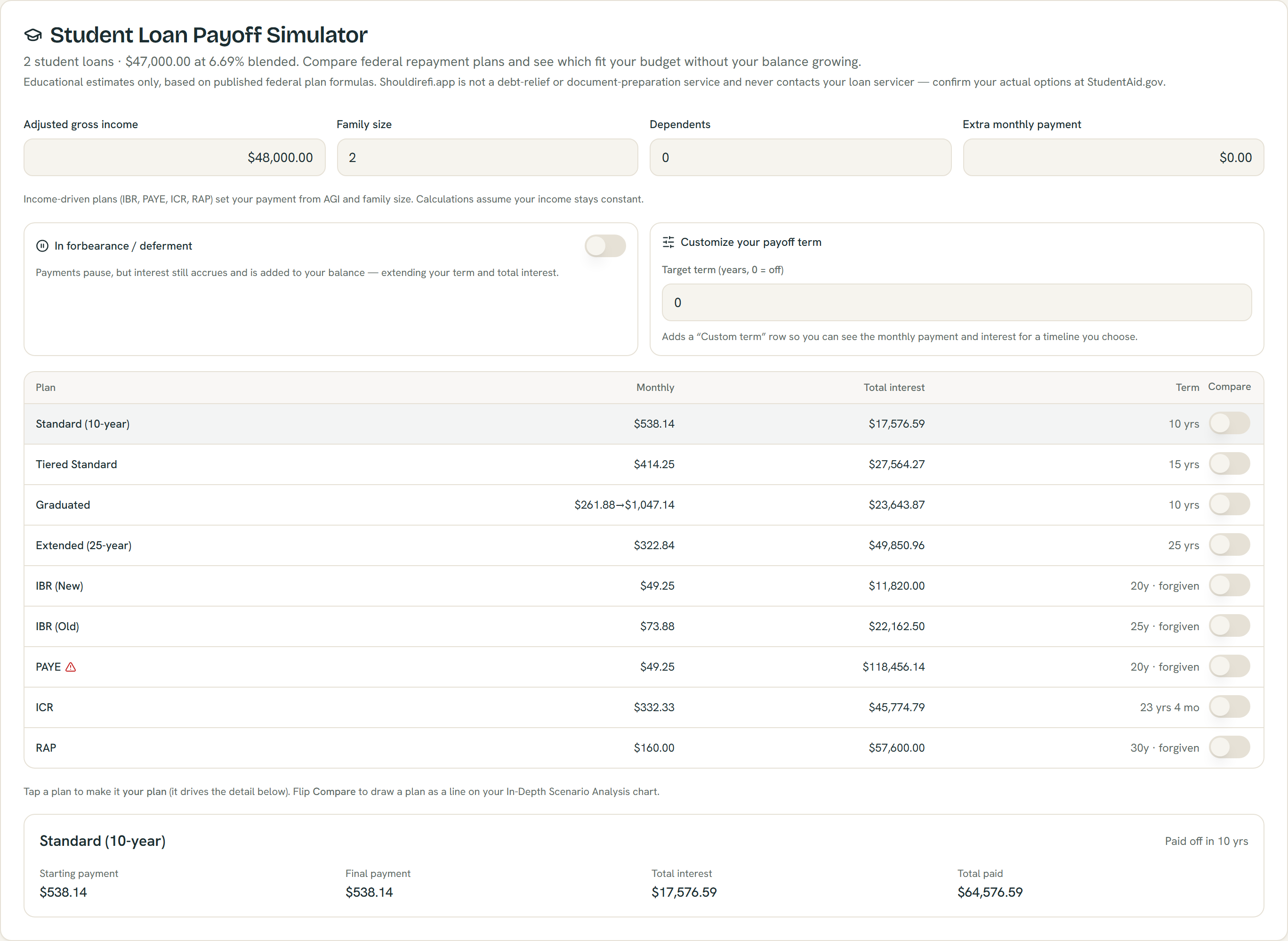

Every federal plan computed at once from example loans, with plans that can grow your balance flagged — educational estimates; confirm your options at StudentAid.gov.

See Your Full Repayment Picture

If you have Parent PLUS loans alongside other student loans or debts, the ShouldIRefi Student Loan Simulator can help you understand the combined picture.

Try the Student Loan Simulator → (https://shouldirefi.app/tool/calculator)

Enter your student loans (marking Parent PLUS loans appropriately), and the app flags which repayment plans you're eligible for — and which ones you're not. You can model ICR, IBR, and fixed-payment options side by side to see which produces the lowest total cost or the most manageable monthly payment.

See your options → (https://shouldirefi.app/tool/calculator)