If you're carrying debt — credit cards, auto loans, or a mix of both — you have two main paths to paying it off without home equity: take out a personal loan to consolidate everything, or pay it down yourself using your existing income.

Both can work. The right choice depends on your interest rates, your discipline, and how quickly you want to be debt-free.

Here's how to think through both options.

What Is Self-Pay?

Self-pay (sometimes called accelerated debt paydown) means you keep paying your existing debts — but you add extra payments each month to pay them off faster. No new loan. No consolidation. Just applying more of your income to the debt you already have.

You can use strategies like:

- Snowball — Pay smallest balance first, build momentum

- Avalanche — Pay highest interest rate first, save the most in interest

- Extra monthly payment — Simply throw a set extra amount at your highest-priority debt each month

Advantages:

- No origination fees

- No credit inquiry

- Complete flexibility — increase, decrease, or pause extra payments as life changes

- No risk of trading a lower payment for a longer payoff period

Disadvantages:

- You're still paying your original high interest rates

- Requires consistent discipline over months or years

- Juggling multiple accounts and due dates can get complicated

What Is a Personal Loan for Debt Consolidation?

A personal loan lets you borrow a fixed amount — typically from $1,000 to $100,000 — at a fixed interest rate, and use the funds to pay off your existing debts. You then make one monthly payment on the personal loan until it's paid off.

Advantages:

- One simple monthly payment instead of many

- Potentially lower interest rate than credit cards (average personal loan APRs run significantly lower than the 20%+ average for credit cards)

- Fixed payoff date — you know exactly when you'll be debt-free

- Can accelerate payoff if the lower rate frees up extra cash each month

Disadvantages:

- Origination fees of 1–8% in some cases

- Requires good credit to get the best rates — damaged credit may mean a rate as high as what you're already paying

- Fixed payments mean less flexibility than self-pay if income changes

- Doesn't address spending habits — you could run the cards back up

When a Personal Loan Wins

A personal loan tends to make more sense when:

- Your existing debts carry high interest rates (especially multiple credit cards at 18–25%+)

- You can qualify for a personal loan at a meaningfully lower rate

- You want the discipline of a fixed payoff schedule with a clear end date

- The interest savings outweigh any origination fees

Example: You have $20,000 in credit card debt at an average of 22% APR. You qualify for a personal loan at 11%. The interest savings over 4 years could be thousands of dollars — and you'll be debt-free on a specific date.

When Self-Pay Wins

Self-pay tends to make more sense when:

- Your existing interest rates are already moderate, and a personal loan won't offer a big enough rate reduction to be worth the fees

- Your credit score would result in a personal loan rate close to what you're already paying

- You have the discipline to stick to a payoff plan without a formal loan structure

- You need flexibility — self-pay can be paused or adjusted if your income changes

The Middle Path: Extra Payments on Your Highest-Rate Debt

Even without a personal loan, putting just $100–$200 more per month toward your highest-interest debt can dramatically shorten your payoff timeline and cut your total interest. This requires no fees, no credit inquiry, and no new loan.

No home required: the same side-by-side comparison works for renters — example figures; estimates only.

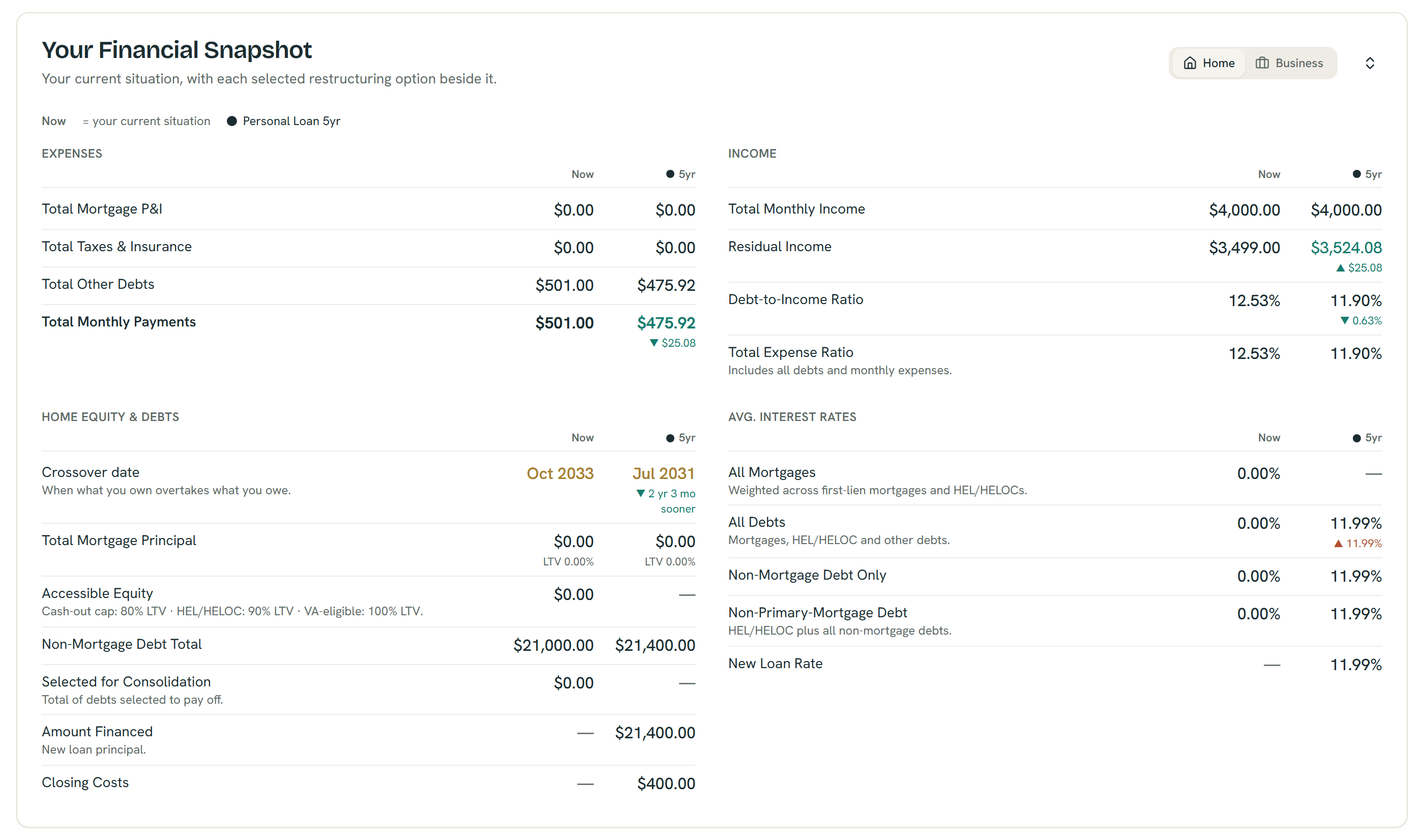

See Which Approach Works for Your Numbers

Here's the truth: the math is different for everyone. The same strategy that saves one person thousands could barely move the needle for another, depending on their debt amounts, interest rates, and monthly budget.

Try the ShouldIRefi Calculator → (https://shouldirefi.app/tool/calculator)

The calculator shows both approaches side by side for your specific situation:

- Your current situation — total interest paid, monthly payments, payoff timeline

- A personal loan scenario — enter a rate and term to see how consolidation changes the picture

- A self-pay scenario — model extra monthly payments and see how much faster you'd be debt-free

You can adjust the numbers in real time and find the combination that actually works for your budget.

Try it free → (https://shouldirefi.app/tool/calculator)

Not sure what numbers to use? Take the Financial Audit (https://shouldirefi.app/tool/audit) — it walks you through your full financial picture step by step.