Refinancing your mortgage can save you a lot of money — but it's not free. There are closing costs to pay upfront, and it takes time before the monthly savings start to add up. That's where the break-even point comes in.

If you've ever wondered "Is refinancing actually worth it?" — the break-even point gives you a real answer. And it's simpler to understand than you might think.

What Is the Break-Even Point?

The break-even point is the moment when the money you've saved from refinancing finally covers what you paid to do it.

Before that point, you're still in the hole. After that point, every month is pure savings.

Simple example:

- You pay $6,000 in closing costs to refinance

- Your new monthly payment is $200 less than your old one

- It takes 30 months to break even ($6,000 ÷ $200 = 30 months)

After 30 months — or 2.5 years — you start actually saving money. Before that, you've technically lost money compared to not refinancing at all.

Why Does It Matter?

The break-even point matters most when you think about how long you plan to stay in your home.

- If you plan to stay for 10 more years and break even in 2 years — refinancing is probably a great move.

- If you plan to sell or move in 18 months and break even takes 30 months — refinancing could cost you money.

This is the #1 mistake people make when refinancing: they focus on the lower monthly payment and forget to ask how long it takes to actually come out ahead.

How to Calculate Your Break-Even Point

You only need two numbers:

- Total closing costs — What you'll pay to get the new loan (lender fees, appraisal, title insurance, etc.). Closing costs are typically 2–6% of the loan amount.

- Monthly savings — The difference between your current monthly payment and your new one.

The formula:

Closing Costs ÷ Monthly Savings = Break-Even in Months

Example:

- Closing costs: $8,000

- New payment: $1,350/month

- Old payment: $1,575/month

- Monthly savings: $225

- Break-even: $8,000 ÷ $225 = about 35 months (just under 3 years)

What Goes Into Closing Costs?

When you refinance, closing costs typically include:

- Origination fee — charged by the lender to process your loan

- Appraisal fee — to confirm your home's value

- Title insurance — protects against ownership disputes

- Recording fees — paid to the local government

- Prepaid items — like property taxes and homeowner's insurance held in escrow

These vary by lender, loan size, and location — which is why it pays to shop around and compare real numbers before committing.

Break-Even on a Cash-Out Refinance

If you're doing a cash-out refinance (pulling equity out of your home), the break-even calculation gets a little more complex. Your new loan is larger, so your payment might not go down much — or it could even go up slightly.

In that case, the break-even isn't just about the monthly payment. It also depends on what you do with the cash. For example:

- If you use it to pay off high-interest credit card debt, you might save more in interest on those debts than you spend on the refinance.

- If you invest the money, you'd compare investment growth against the refinance costs.

The break-even on a cash-out refi requires looking at the whole financial picture — not just the mortgage payment.

How Long Is Too Long to Break Even?

There's no single right answer, but a few common guidelines:

- Under 2 years — Usually a clear win, especially if you're staying in the home long-term

- 2–4 years — Solid if you're confident you're not moving

- 4–7 years — Depends on your plans; worth thinking carefully

- 7+ years — Tread carefully unless you're certain you'll stay

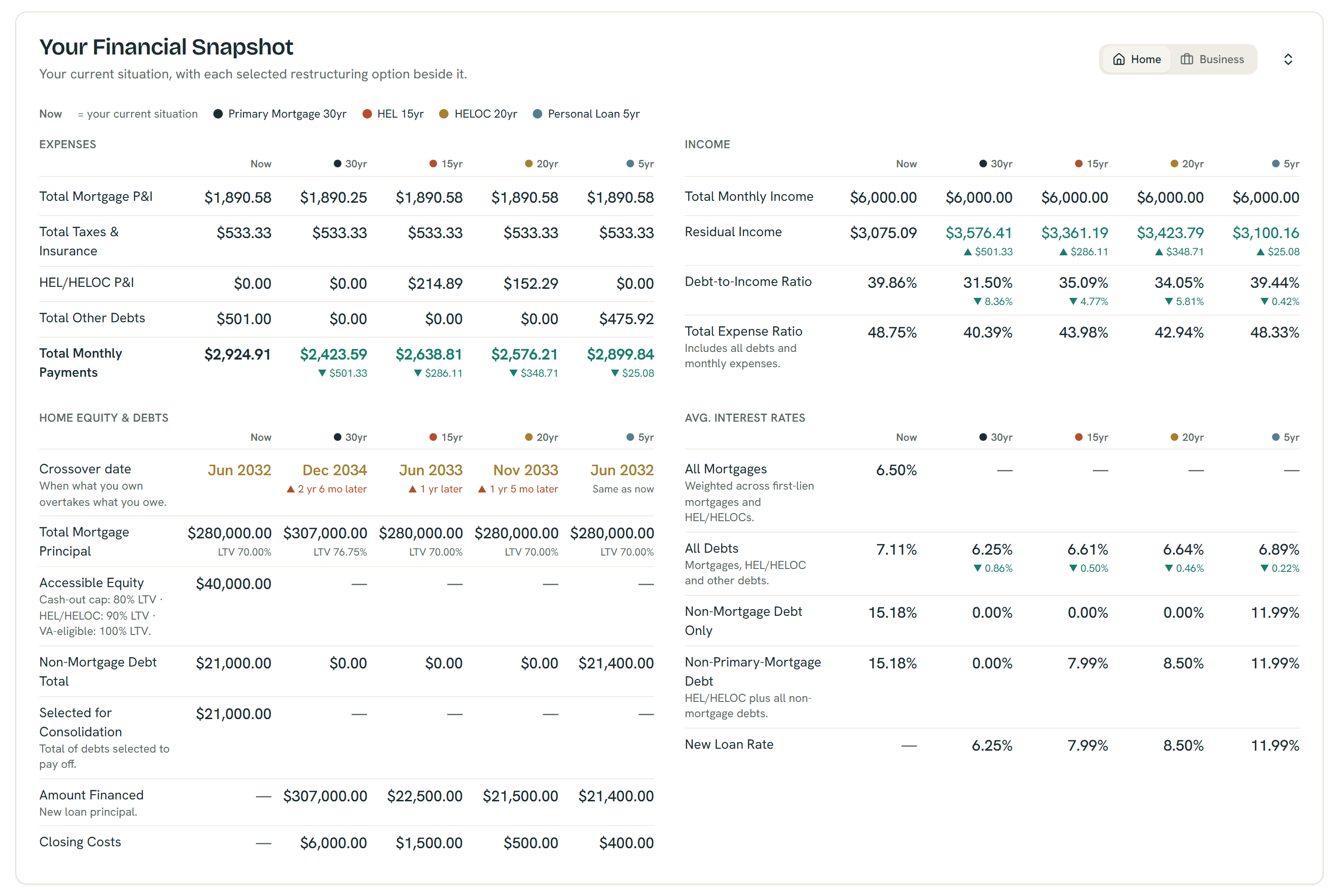

The Financial Snapshot puts every option beside your current numbers — example figures shown; all outputs are estimates, not quotes or offers.

See Your Real Break-Even Point in Seconds

You don't have to do the math by hand. The break-even point is one of the main outputs in the ShouldIRefi Calculator (https://shouldirefi.app/tool/calculator).

Enter your current mortgage details, a potential new rate and term, and any closing costs — and the app shows you exactly how many months until you break even. You can also compare multiple scenarios side by side (cash-out refi, HELOC, home equity loan) to see which approach gets you to savings the fastest.

Try it free → (https://shouldirefi.app/tool/calculator)

Not sure what numbers to enter? Start with the Financial Audit (https://shouldirefi.app/tool/audit) — it walks you through your full picture step by step and loads everything into the calculator automatically.