If you own a home and you're carrying credit card balances, auto loans, or other high-interest debt, you already have something most people don't: a powerful tool to knock that debt out fast and at a fraction of the interest rate.

Home equity — the portion of your home you actually own — can be borrowed against in three different ways: a cash-out refinance, a home equity line of credit (HELOC), or a home equity loan (HEL). All three can wipe out high-interest debt and dramatically lower what you're paying each month. The question is which one wins for your specific situation.

Why Using Home Equity Makes So Much Sense for Debt Payoff

Credit cards routinely charge 20–25% interest. Auto loans often run 7–12%. Mortgage-based borrowing — whether a cash-out refi, HELOC, or home equity loan — typically comes in well under 10%.

That gap is the opportunity. Replacing high-rate debt with home equity financing means more of your monthly payment goes to actually reducing what you owe instead of feeding interest charges. The savings over time can be substantial — often tens of thousands of dollars, depending on how much debt you're carrying.

And unlike other debt payoff strategies, all three home equity options can give you real, immediate relief on your monthly cash flow.

Option 1: Cash-Out Refinance

A cash-out refinance replaces your existing mortgage with a new, larger one. The difference comes to you in cash at closing, which you use to pay off your other debts. You're left with one single mortgage payment.

Example:

- Current mortgage balance: $250,000

- Home value: $400,000

- New loan: $310,000 (within the 80% LTV cap)

- Cash received at closing: ~$60,000

- Result: Credit cards, car loan, and other debts paid off — one new mortgage payment each month

Why a cash-out refi often wins:

The biggest advantage is consolidation. Everything — your original mortgage and all your other debts — rolls into a single payment. If your new mortgage rate is competitive, this can be the lowest total monthly obligation of any option.

A cash-out refi also locks in a fixed rate on your entire debt load. There's no variable rate risk, no separate second payment, and no draw period to navigate. For borrowers who value simplicity and predictability, that's a real benefit.

Cash-out refis tend to make the most sense when:

- You can get a competitive rate on the new mortgage

- The consolidation of all debts into one payment meaningfully lowers your monthly total

- You plan to stay in the home long enough to recoup closing costs (typically 2–5% of the loan amount)

- Your existing mortgage rate is already relatively high, so the rate on the cash-out refi is close to or better than what you have now

Option 2: HELOC (Home Equity Line of Credit)

A HELOC leaves your existing mortgage completely untouched and opens a separate revolving line of credit based on your equity. You draw from it as needed, make monthly payments during the draw period (typically interest-only on your current balance), and repay the remaining balance over the following 10–20 years.

Why a HELOC can be the right call:

If you locked in a great mortgage rate and don't want to give it up, a HELOC is the way to access equity without touching your first mortgage. You only pay interest on what you actually borrow, and rates are often lower than credit cards by a wide margin.

HELOCs work especially well for debt that you want to pay off aggressively in a shorter period — the flexibility to make larger payments and pay it down fast can save a lot in interest.

HELOCs tend to make the most sense when:

- Your existing mortgage rate is low and worth protecting

- You have a clear plan to pay off the balance within the draw period

- You want flexibility to borrow only what you need

- You're comfortable with a variable rate (most HELOCs are adjustable)

Option 3: Home Equity Loan (HEL)

A home equity loan also leaves your first mortgage alone and adds a second loan — but unlike a HELOC, it gives you a lump sum at a fixed rate with predictable monthly payments from day one. You know exactly what you owe and exactly when it's paid off.

Why a HEL can be the right call:

If you want the protection of a fixed rate on your second loan (rather than the variable rate of a HELOC) while keeping your original mortgage intact, a home equity loan hits the sweet spot. It's especially useful when you know the exact amount you need to pay off and want structured, predictable payments.

HELs tend to make the most sense when:

- You want a fixed rate and consistent payment on your second lien

- You know exactly how much you need to borrow

- Your first mortgage rate is worth keeping

- You prefer not to manage a revolving credit line

The Weighted Average Rate: The Key to Comparing Options

Here's a concept that can make the decision much clearer.

When you're comparing a cash-out refinance against keeping your existing mortgage and adding a HELOC or HEL, you're not just comparing two interest rates — you're comparing the combined cost of two loans against one.

The way to do that fairly is to calculate the weighted average interest rate of the HELOC or HEL combined with your existing mortgage, then compare that to the cash-out refi rate.

How to calculate the weighted average:

Weighted Rate = (Mortgage Balance × Mortgage Rate + Second Loan Balance × Second Loan Rate) ÷ Total Combined Balance

Example:

- Existing mortgage: $250,000 at 4.5%

- HELOC to pay off debt: $60,000 at 8.5%

- Total combined balance: $310,000

Weighted average = ($250,000 × 4.5% + $60,000 × 8.5%) ÷ $310,000 = ($11,250 + $5,100) ÷ $310,000 = $16,350 ÷ $310,000 = 5.27%

Now compare that to a cash-out refinance rate of, say, 6.5% on $310,000.

The weighted average on the HELOC + existing mortgage is lower (5.27% vs. 6.5%), so purely on interest rate, keeping the existing mortgage and adding the HELOC wins.

But here's where it gets interesting.

Even if the cash-out refi has a higher rate, the monthly payment can still be lower — because the refi typically uses a 30-year term, while a HELOC or HEL repayment period is often 10–20 years on a larger portion of the balance.

When the rates are close but the cash-out refi has a lower monthly payment, the refi is often the better practical choice. The extra interest from the slightly higher rate may be more than offset by the lower monthly obligation — and the simplicity of a single payment is worth something too.

This is exactly why you can't just compare rates in isolation. The monthly payment, the loan terms, and how long you plan to stay in the home all matter.

A Simple Decision Guide

| Your Situation | Best Option |

|---|---|

| Current mortgage rate is relatively high | Cash-out refi (consolidate everything at a better rate) |

| Current mortgage rate is low and worth keeping | HELOC or HEL |

| Want one payment, maximum simplicity | Cash-out refi |

| Want to pay off second loan aggressively within 5–10 years | HELOC or HEL |

| Need flexibility to borrow different amounts over time | HELOC |

| Want fixed, predictable second payment | HEL |

| Weighted avg of existing mortgage + second loan is close to refi rate, but refi has lower payment | Cash-out refi often wins |

One Important Consideration on All Three Options

All three home equity strategies turn what were once separate debts into obligations secured by your home. That's not a reason to avoid them — it's just something to go in eyes open about. The interest savings are real and often substantial. The key is making sure the new payment is genuinely manageable within your monthly budget.

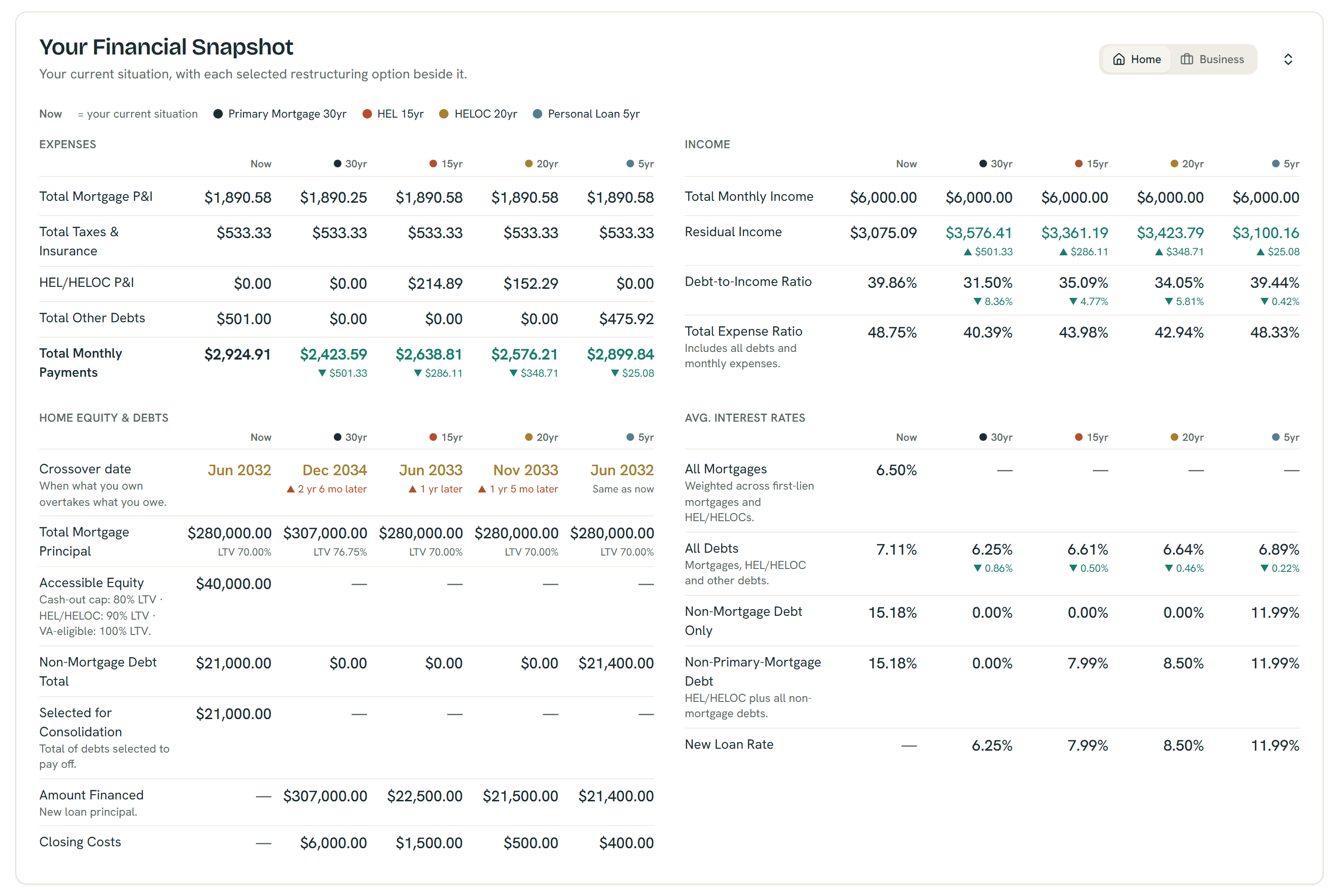

The Financial Snapshot puts every option beside your current numbers — example figures shown; all outputs are estimates, not quotes or offers.

See All Three Options Side by Side

The math is different for every homeowner. The same cash-out refi that makes obvious sense for one person might lose to a HELOC by a wide margin for another — it all depends on your current rate, your home value, your debts, and your goals.

Try the ShouldIRefi Calculator → https://shouldirefi.app/tool/calculator

You can model a cash-out refinance, HELOC, and home equity loan simultaneously and compare them against each other — and against your current situation. The calculator shows monthly savings, total interest, break-even months, and 30-year equity projections for each scenario. It also calculates weighted average rates across your debt so you can see the full picture clearly.

Run your comparison → https://shouldirefi.app/tool/calculator

Not sure where to start? Take the Financial Audit → https://shouldirefi.app/tool/audit — it walks through your full financial picture step by step and loads everything into the calculator automatically.