When money gets tight, forbearance sounds like a lifeline: pause your student loan payments for a while and catch your breath.

But there's a catch most borrowers don't fully understand until it's too late.

During forbearance, interest keeps building on your loans — and when forbearance ends, that interest may get added to your principal balance.

Here's what that really means for you.

What Is Forbearance?

Forbearance is a temporary pause (or reduction) in your federal student loan payments. It's typically granted when you're experiencing financial hardship, a change in employment, medical expenses, or another qualifying difficulty.

There are two main types:

- General forbearance — Requested from your loan servicer. Approval is not guaranteed. Typically granted for up to 12 months at a time, with a cumulative limit of 3 years.

- Mandatory forbearance — Required by law when you meet specific conditions, such as serving in the National Guard, completing a medical residency, or participating in national service.

What Happens to Interest During Forbearance?

This is the part that surprises many borrowers.

During forbearance, interest accrues on ALL loan types — including subsidized loans.

This is different from deferment, where subsidized loans don't accrue interest during the pause.

With forbearance:

- Your monthly payments stop

- Interest keeps building, every day

- When forbearance ends, the accrued interest may be capitalized — meaning it gets added to your principal balance

What capitalization means: Once unpaid interest is added to your principal, you start paying interest on a larger balance. Interest accruing on interest. This can meaningfully increase the total cost of your loan.

Example: You have $35,000 in student loans at 6.39% interest. You enter forbearance for 12 months.

- Monthly interest accrual: roughly $186

- After 12 months: about $2,232 in unpaid interest

- If capitalized, your new balance becomes approximately $37,232 — and you now pay interest on that larger amount for the rest of your loan term

Forbearance vs. Deferment: What's the Difference?

Both pause required payments, but they're not the same:

| Forbearance | Deferment | |

|---|---|---|

| Interest on subsidized loans | Accrues | Does NOT accrue |

| Interest on unsubsidized loans | Accrues | Accrues |

| Counts toward IDR forgiveness | No | Depends on type |

| Counts toward PSLF | No | Depends on type |

| Eligibility | Broader, sometimes discretionary | Specific qualifying circumstances |

If you qualify for deferment, it's almost always the better option — particularly for subsidized loans.

A Better Alternative: Income-Driven Repayment

Here's something many borrowers don't know: income-driven repayment plans (like IBR and RAP) can set your payment as low as $0 based on your income and family size.

A $0 payment on an income-driven plan is very different from forbearance:

- Months with $0 IDR payments count toward forgiveness timelines (including PSLF in many cases)

- Months in general forbearance do NOT count toward forgiveness

- On RAP (available July 2026), unpaid interest is waived — your balance won't grow even at $0 payments

If you're struggling to make payments, exploring IDR plans before turning to forbearance could save you years of repayment time and thousands in interest.

When Forbearance Makes Sense

Despite these drawbacks, forbearance does have its place:

- Short-term emergencies where you need immediate payment relief and don't have time to process an IDR application

- Situations where you're between plans or waiting for IDR processing

- Cases where you've used up deferment eligibility

The key is to treat it as a temporary bridge, not a long-term solution — and to switch to a more appropriate repayment plan as soon as possible.

Upcoming Changes: Forbearance Is Getting More Restricted

For borrowers who take out new loans on or after July 1, 2027, forbearance limits will tighten significantly under changes passed in 2025. General forbearance will be capped at 9 months within any 24-month period (down from 12 months per year). Economic hardship and unemployment deferments will no longer be available for these newer loans.

If you already have federal student loans, existing protections remain in place.

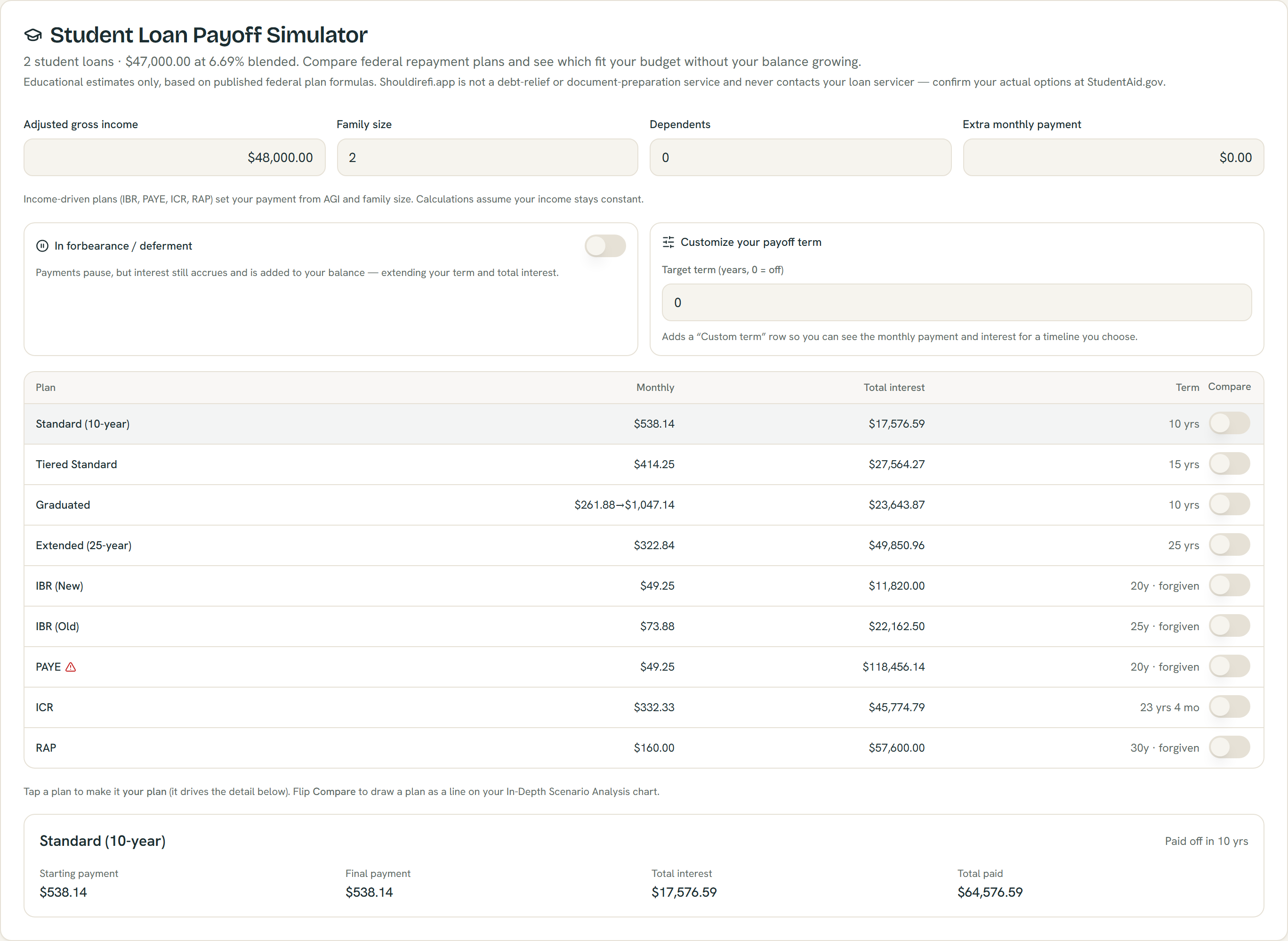

Every federal plan computed at once from example loans, with plans that can grow your balance flagged — educational estimates; confirm your options at StudentAid.gov.

See How Forbearance Affects Your Total Cost

The ShouldIRefi Student Loan Simulator lets you model forbearance directly.

Try the Student Loan Simulator → (https://shouldirefi.app/tool/calculator)

Toggle the forbearance setting, enter how many months you've paused (or plan to pause), and the app recalculates your loan balance, total interest, and repayment timeline across all federal plans. You can compare what forbearance costs you versus switching to an income-driven plan with a $0 payment — and see which decision saves more in the long run.

Model your forbearance → (https://shouldirefi.app/tool/calculator)