If you own a home and you're carrying credit card debt at 20% interest or higher, you're in a situation worth fixing immediately. You're sitting on an asset — your home equity — that you can borrow against at a fraction of the rate you're currently paying on those cards.

This isn't a complicated strategy. It's one of the most straightforward moves in personal finance: replace expensive debt with cheap debt, and keep the difference every month.

The Math Is Compelling

Credit cards typically charge 20–25% APR or higher. Home equity products — cash-out refinances, HELOCs, and home equity loans — generally come in well under 10% for qualified borrowers.

That spread is the opportunity. On $30,000 in credit card debt at 22%, you're paying roughly $550 a month in interest charges alone — much of which never reduces your balance. Replace that debt with a home equity product at 8%, and the interest drops dramatically. The savings compound every month you carry the balance.

Beyond the rate savings, you also go from juggling multiple credit card minimums, due dates, and balances to a single, structured payment. That clarity alone makes it easier to stay on track and actually get out of debt.

Three Ways to Do It

Option 1: Cash-Out Refinance

A cash-out refinance replaces your existing mortgage with a new, larger one. The difference comes to you as a lump sum at closing, which you use to pay off the credit cards in full. You're left with one mortgage payment covering everything.

This works especially well when you can get a competitive rate on the new mortgage — particularly if your current rate is already on the higher side. You simplify your entire debt picture into one payment at one rate, and if that payment is lower than what you were paying on the mortgage plus the credit cards combined, the math is obvious.

Closing costs (typically 2–5% of the loan amount) are the main upfront cost to factor in, but for borrowers with significant credit card balances, the monthly savings often recover those costs within a year or two.

Option 2: Home Equity Loan (HEL)

A home equity loan leaves your existing mortgage completely alone and adds a second loan on top of it — a fixed amount at a fixed rate, paid back over a set term. You use the lump sum to clear the credit cards, then make one predictable second payment each month.

This is an excellent option when your existing mortgage has a low rate you don't want to touch. The home equity loan rate will be higher than your first mortgage rate, but it's still dramatically lower than credit card rates — and unlike a HELOC, the payment never changes.

Option 3: HELOC (Home Equity Line of Credit)

A HELOC also leaves your first mortgage untouched and opens a revolving credit line based on your equity. You draw what you need, pay down the credit cards, and repay the HELOC over time — with payments during the draw period typically based only on what you've actually borrowed.

HELOCs are especially useful if you're carrying debt across several cards and want the flexibility to pay them off in stages, or if you want to keep access to credit as a financial cushion after you've paid down the balances. The variable rate is something to be aware of, but even at higher variable rates, a HELOC almost always beats credit card APRs.

How to Choose Between the Three

The right option depends mainly on your existing mortgage rate and how much you value simplicity versus flexibility.

Choose a cash-out refinance if:

- Your current mortgage rate isn't significantly lower than today's rates

- You want everything — mortgage and credit card debt — consolidated into one payment

- A single payment at the new rate is meaningfully lower than your current combined obligations

- You're comfortable with the closing costs relative to your balance

Choose a home equity loan if:

- Your existing mortgage rate is low and worth keeping

- You want a fixed rate and payment on the second loan

- You know exactly how much you need to borrow

- You prefer a clear, structured payoff timeline

Choose a HELOC if:

- Your existing mortgage rate is low and worth keeping

- You want flexibility to draw and repay over time

- You're comfortable with a variable rate

- You like having a credit line available after paying down the cards

How Do These Compare to Other Options?

Personal loan: A personal loan requires no home equity and no collateral — which is its main advantage for people who don't own a home. For homeowners, though, personal loan rates are typically higher than home equity rates, sometimes significantly, since the lender has no asset backing the loan. If you have equity, a home equity product almost always beats a personal loan on rate.

Balance transfer credit card: Some cards offer a 0% introductory APR for 12 to 21 months. That sounds attractive, but there are two important catches: the transfer usually costs 3–5% of the balance upfront as a fee, and once the intro period ends, the rate jumps to the card's standard APR — which could be just as high as what you started with. A 0% balance transfer can make sense for smaller balances you're confident you can pay off entirely within the promotional window. For larger balances or longer payoff horizons, a home equity product offers a lower and more sustainable rate over the full term.

Self-pay (avalanche or snowball): Paying down credit cards with existing income is always an option, and for smaller balances it can work well. The downside is that you're paying the full credit card rate the entire time, which slows progress considerably on larger balances. Home equity financing lets you cut the rate immediately and redirect more of each payment toward actually reducing the principal.

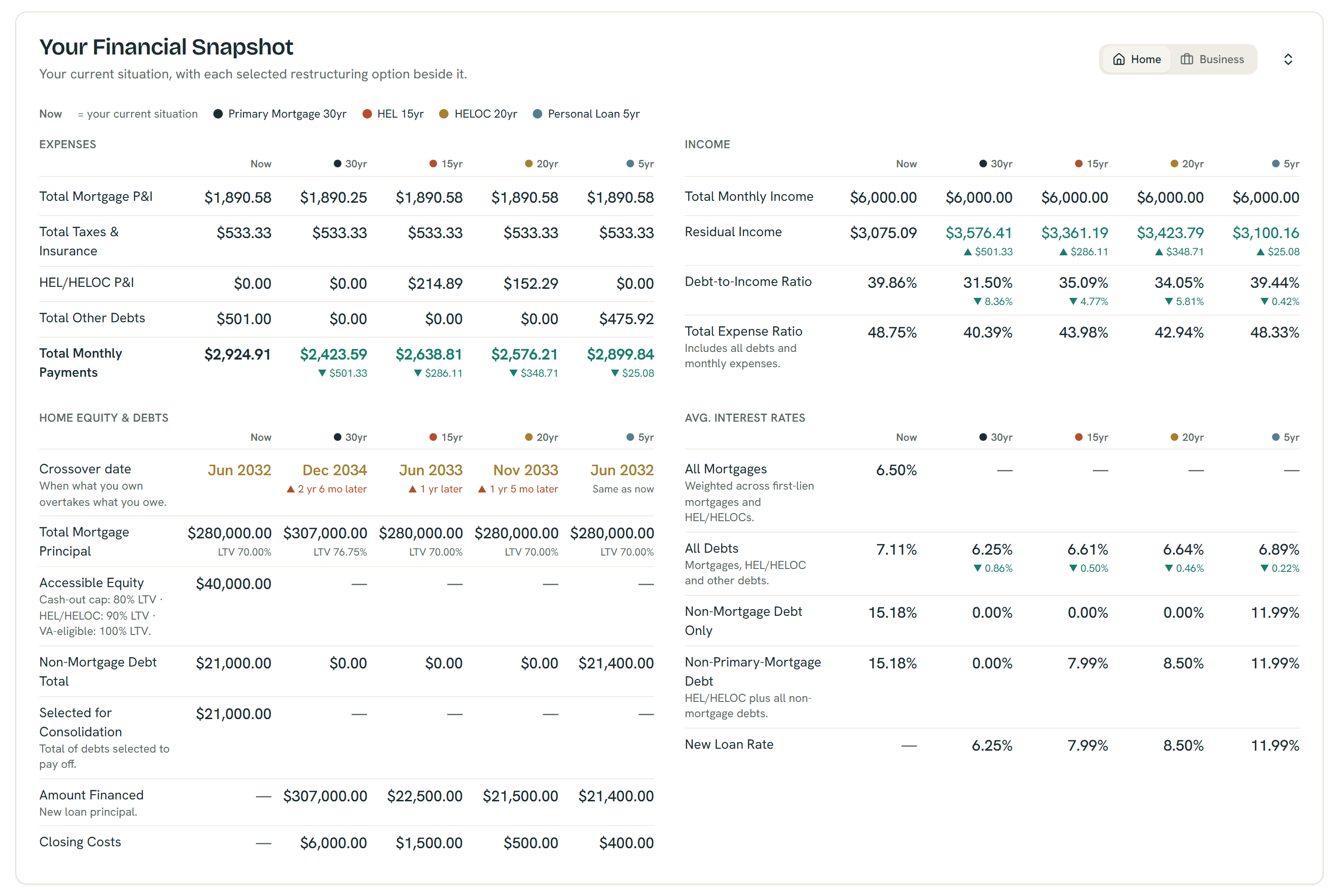

The Financial Snapshot puts every option beside your current numbers — example figures shown; all outputs are estimates, not quotes or offers.

Choosing the Right Fit for Your Numbers

The best way to know which option wins for your specific situation is to run the actual numbers — your equity, your credit card balances, your current mortgage rate, and what rates are available to you today.

Try the ShouldIRefi Calculator → (https://shouldirefi.app/tool/calculator)

You can model a cash-out refinance, HELOC, and home equity loan side by side — and compare all three against your current situation and against self-pay. The calculator shows your monthly savings, total interest paid across all debt, break-even on closing costs, and 30-year equity projection for each scenario.

See your numbers → (https://shouldirefi.app/tool/calculator) Want a guided walkthrough first? Take the Financial Audit → (https://shouldirefi.app/tool/audit) — it collects your mortgage, debts, income, and expenses step by step and loads everything into the calculator automatically.