When you apply for a mortgage or refinance, lenders look at a lot of things: your credit score, your income, your home value. But one number that often catches people off guard is their DTI — debt-to-income ratio.

It's one of the most important numbers in your financial picture. And if it's too high, it can stop a loan approval in its tracks — even if everything else looks great.

Here's what it means, how to calculate it, and what you can do about it.

What Is DTI?

DTI is a percentage. It compares how much money you owe in monthly debt payments to how much money you bring in each month.

The formula:

DTI = Total Monthly Debt Payments ÷ Gross Monthly Income × 100

Example:

- Monthly debt payments: $2,000 (mortgage, car loan, credit cards)

- Gross monthly income: $6,000 (before taxes)

- DTI = $2,000 ÷ $6,000 × 100 = 33%

That means 33 cents out of every dollar you earn goes toward debt payments. The rest is available for living expenses, savings, and everything else.

What Counts as "Debt" in the Calculation?

These are typically included in DTI:

- Mortgage or rent payment (or the projected new one)

- Car loans and leases

- Student loan payments

- Credit card minimum payments

- Personal loans

- Child support or alimony

These are not typically included:

- Groceries

- Utilities (electric, gas, water)

- Phone bill

- Insurance

- Childcare

It's only debt obligations — not living expenses.

What DTI Range Do Lenders Want?

Different lenders have different standards, but here are the general guidelines:

| DTI Range | What Lenders See |

|---|---|

| Under 36% | Strong — easy to qualify |

| 36–43% | Acceptable for most loans |

| 43–50% | Possible, but harder — may need strong credit or large down payment |

| Over 50% | Difficult to qualify for most conventional loans |

A common guideline is the 28/36 rule: your housing costs shouldn't exceed 28% of your income, and all your debts combined shouldn't exceed 36%. Most lenders use these as a starting point, though they can go higher for well-qualified borrowers.

Why Do Lenders Care So Much?

DTI tells a lender whether you'll have enough breathing room to handle a new mortgage payment on top of your existing debts.

If most of your income is already spoken for before the mortgage is added, a lender may worry that one unexpected expense — a car repair, a medical bill — could cause you to miss payments.

A lower DTI signals more financial flexibility and less risk. That often means better loan terms, lower rates, and easier approval.

How DTI Affects Refinancing

DTI isn't just for home purchases. When you refinance, lenders run the same calculation — but now they factor in your proposed new mortgage payment instead of your current one.

This matters most if:

- Your new loan will have a higher payment than your current one

- You've taken on more debt since your original mortgage (car loans, credit cards)

- You're doing a cash-out refinance, which increases your loan balance

One of the major benefits of debt consolidation through a refinance is that it can lower your DTI — by paying off high monthly payments (like credit card minimums) and rolling them into a lower mortgage payment.

How to Lower Your DTI

If your DTI is too high, here are the most direct ways to bring it down:

1. Pay off debt Paying off a car loan, credit card, or personal loan reduces your monthly debt total and brings DTI down. Even small wins add up.

2. Increase your income A raise, a second income, or verifiable income from freelance or rental property all increase the denominator in the DTI formula.

3. Consolidate debt at a lower rate Replacing multiple high-payment debts with a single lower-payment loan (like a personal loan or home equity product) can shrink your monthly obligation.

4. Avoid taking on new debt before applying Opening new credit accounts or financing a car right before applying for a mortgage will push your DTI up and could hurt your approval.

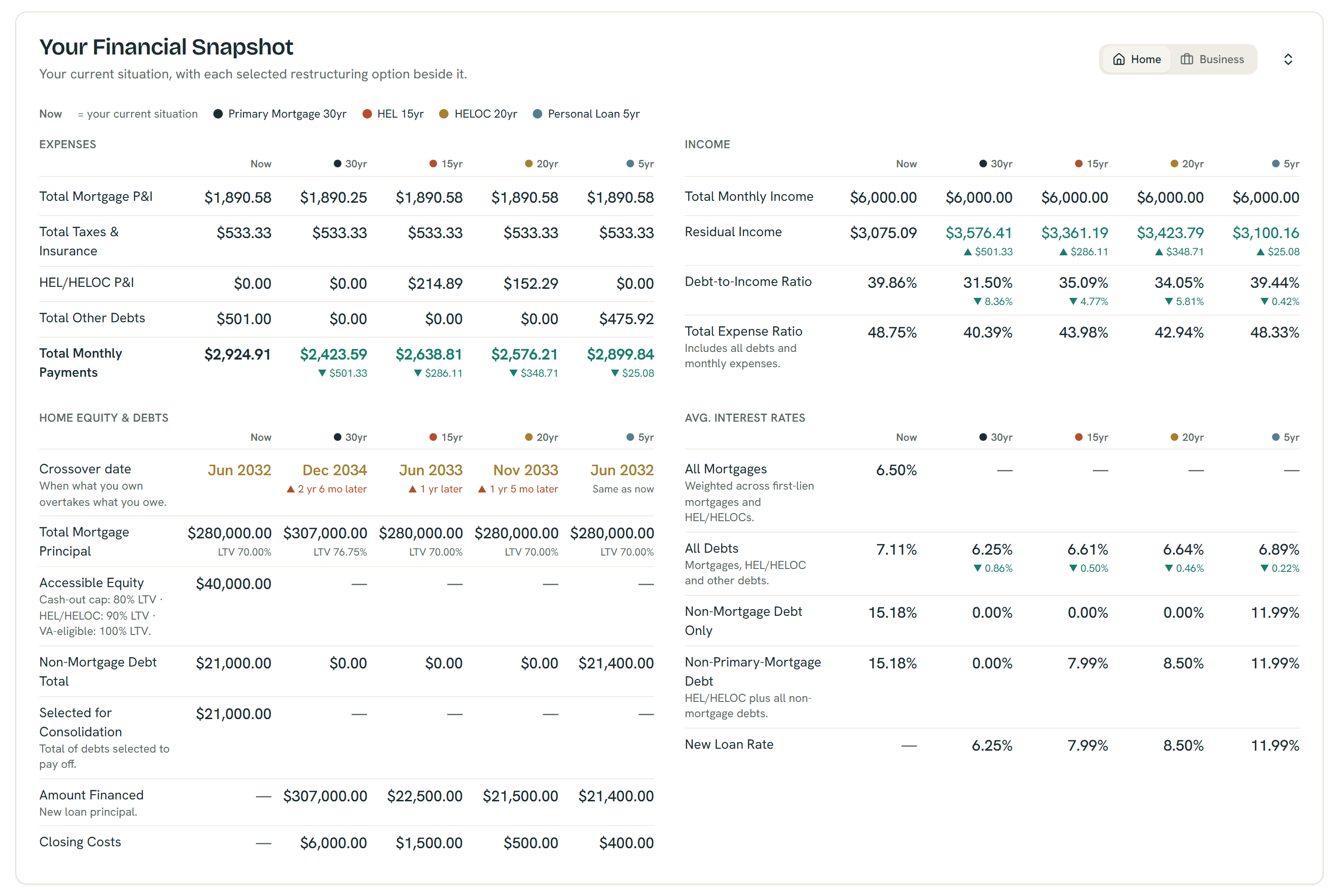

The Financial Snapshot puts every option beside your current numbers — example figures shown; all outputs are estimates, not quotes or offers.

See Your DTI Before You Apply

The ShouldIRefi Calculator shows your DTI in real time — both your current situation and how it would look under different refinance or debt payoff scenarios.

Try the ShouldIRefi Calculator → (https://shouldirefi.app/tool/calculator)

You can model what happens to your DTI if you do a cash-out refinance to pay off credit cards, or if you add a personal loan, or if you simply pay extra each month. The calculator shows your DTI before and after each scenario so you can see the full picture before you talk to a lender.

Not sure where to start? Take the Financial Audit (https://shouldirefi.app/tool/audit) — it walks you through your finances step by step and loads everything into the calculator automatically.