If you've looked into refinancing or pulling equity out of your home, you've probably come across the term LTV. It stands for loan-to-value ratio, and it's one of the biggest factors that determines whether you qualify, what rate you get, and how much cash you can take out.

Once you understand LTV, a lot of things about refinancing and home equity borrowing start to make a lot more sense.

What Does LTV Mean?

LTV compares how much you owe on your home to how much your home is worth.

The formula:

LTV = Loan Balance ÷ Home Value × 100

Example:

- Your home is worth $400,000

- You owe $280,000 on your mortgage

- LTV = $280,000 ÷ $400,000 × 100 = 70%

That means you owe 70% of your home's value, and you own the other 30% free and clear. That 30% is your equity.

The lower your LTV, the more equity you have — and generally, the better your position when it comes to borrowing.

Why Do Lenders Care About LTV?

From a lender's point of view, LTV is a measure of risk. The higher the LTV, the more money the lender has on the line. If you stopped paying your mortgage and the home had to be sold, a lender with a 95% LTV loan would be much more at risk of losing money than one with a 60% LTV loan.

That's why lenders use LTV to:

- Decide whether to approve your loan

- Set your interest rate (lower LTV often means a better rate)

- Determine if you need to pay private mortgage insurance (PMI)

As a rule, if your LTV is above 80%, most conventional lenders will require PMI — an extra monthly cost that protects the lender, not you. Once your LTV drops to 80% or below (through payments or rising home value), you can usually get PMI removed.

LTV and Cash-Out Refinancing

This is where LTV becomes especially important. When you do a cash-out refinance, you're borrowing more than you currently owe and taking the extra as cash. But lenders won't let you borrow more than a certain percentage of your home's value.

Most conventional lenders cap cash-out refinancing at 80% LTV.

That means your new loan amount can't exceed 80% of your home's appraised value.

Example:

- Home value: $500,000

- 80% LTV cap: $400,000

- Current mortgage balance: $300,000

- Maximum cash-out: $400,000 − $300,000 = $100,000

Even if you have $200,000 in equity on paper, lenders typically won't let you borrow all of it — they require you to leave at least 20% equity in the home.

VA loans are different. If you're a veteran or active-duty service member, VA cash-out refinance loans allow up to 100% LTV — meaning you can potentially borrow all the way up to the full appraised value of your home.

LTV and HELOCs / Home Equity Loans

LTV also limits how much you can borrow through a HELOC or home equity loan. Lenders look at your combined loan-to-value (CLTV) — which adds up all the money you owe on the home, including your first mortgage and any second loans.

Example:

- Home value: $400,000

- First mortgage: $250,000

- HELOC limit at 80% CLTV: $320,000 − $250,000 = $70,000 available to borrow

If you've paid down your mortgage significantly, or if your home has gone up in value, your CLTV may be low enough to open up a meaningful line of credit.

How to Know Your LTV Right Now

Two things you need:

- Your current mortgage balance — check your most recent statement

- Your home's current value — this is the trickier number; it may have changed since you bought

Home values can go up or down over time. If your neighborhood has appreciated, your LTV may be lower (better) than you think — which could mean more equity to tap than you expected.

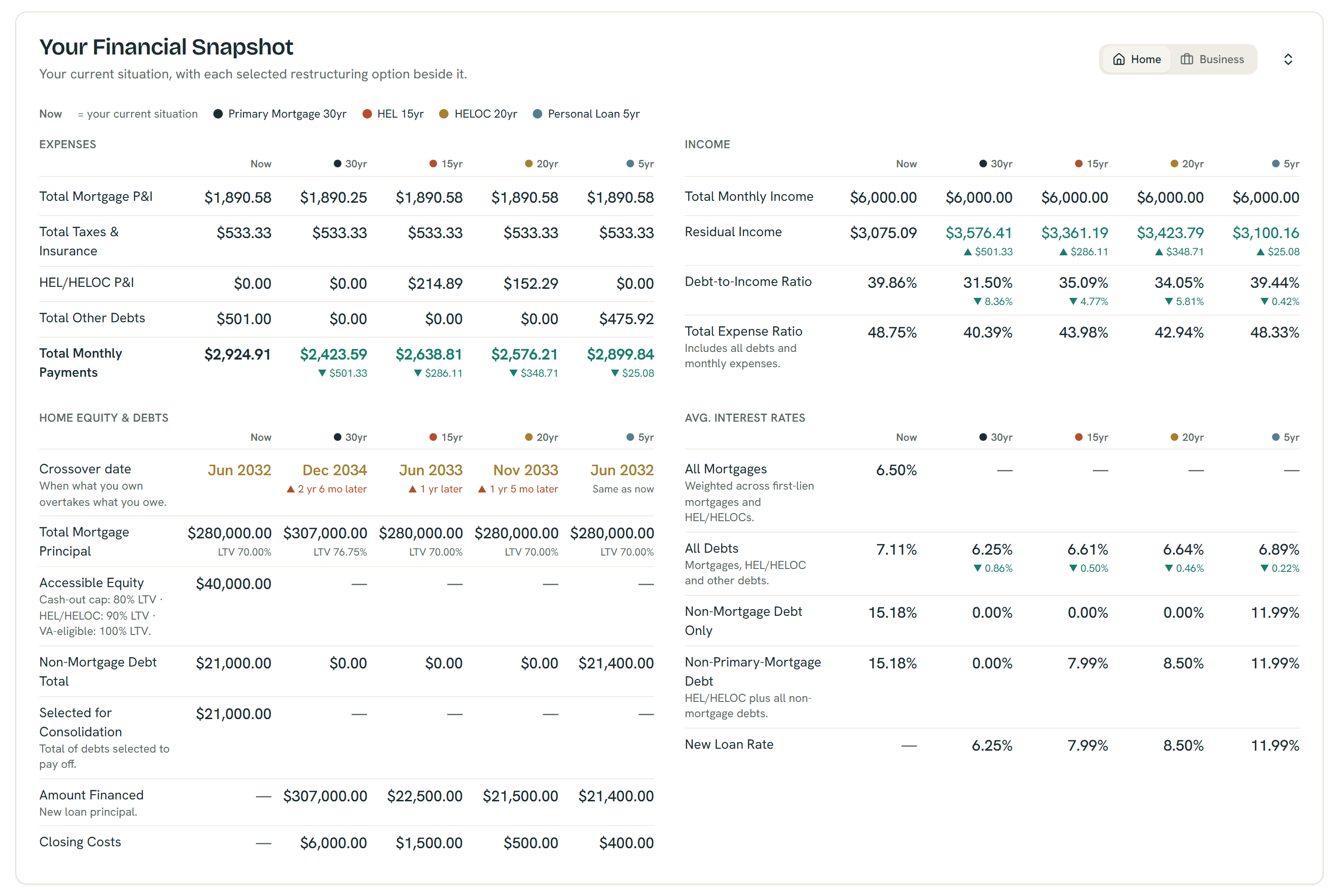

The Financial Snapshot puts every option beside your current numbers — example figures shown; all outputs are estimates, not quotes or offers.

Why LTV Matters in Your Scenario Planning

When you're weighing different options — cash-out refi, HELOC, home equity loan — your LTV determines which ones you can actually use and how much you can access through each. A scenario that looks great on paper might not be available to you if your LTV is too high.

That's why it helps to model your actual numbers before making any decisions.

Try the ShouldIRefi Calculator → (https://shouldirefi.app/tool/calculator)

Enter your home value, mortgage balance, and debts, and the app automatically calculates your LTV, shows what's available to you under each financing option, and flags if any LTV cap prevents you from fully consolidating your debt. It also models VA loan mode if that applies to you.

Not sure where to start? Take the Financial Audit (https://shouldirefi.app/tool/audit) for a step-by-step guided walkthrough that loads everything into the calculator automatically.