Ask what a small business is worth and you'll hear "a multiple of earnings." The trap is that earnings means two different things depending on the business's size — and the multiples attached to each are not comparable yardsticks.

SDE: the owner-operator's number

Seller's Discretionary Earnings = net income + interest + taxes + depreciation/amortization + the owner's salary + perks + one-time expenses.

It answers: if one person owned and ran this business, what's the total economic benefit they'd collect? Salary, distributions, the truck, the phone plan — all of it. SDE is the pricing metric in the vast majority of Main Street transactions (one industry source puts it above 90% of deals under $5M). Typical range: 2–4× SDE, median around 2.6–2.7×.

EBITDA: the investor's number

Adjusted EBITDA starts the same way but then subtracts a market-rate salary for a manager to run the business without you. It answers: what does this business earn as a standalone machine? It applies to larger, management-run businesses — typically $1M–$2M+ in earnings — and trades at higher multiples: roughly 3–6× for small companies, more for recurring-revenue businesses.

The relationship (and the trap)

Same business, two lenses:

SDE − market-rate manager salary ≈ EBITDA

A business with $1,000,000 of SDE might show $700,000 of EBITDA after a $300K general manager. Now watch the trap: a seller hears "software companies trade at 6×," applies it to their SDE, and lists at $6M — when 6× was an EBITDA multiple and the honest number is $700K × 6 = $4.2M. Or a buyer compares a 2.8× SDE deal against a "5× industry average" that was quoted on EBITDA and thinks they've found a bargain.

The rule: never compare a multiple without knowing which earnings basis it's quoted on.

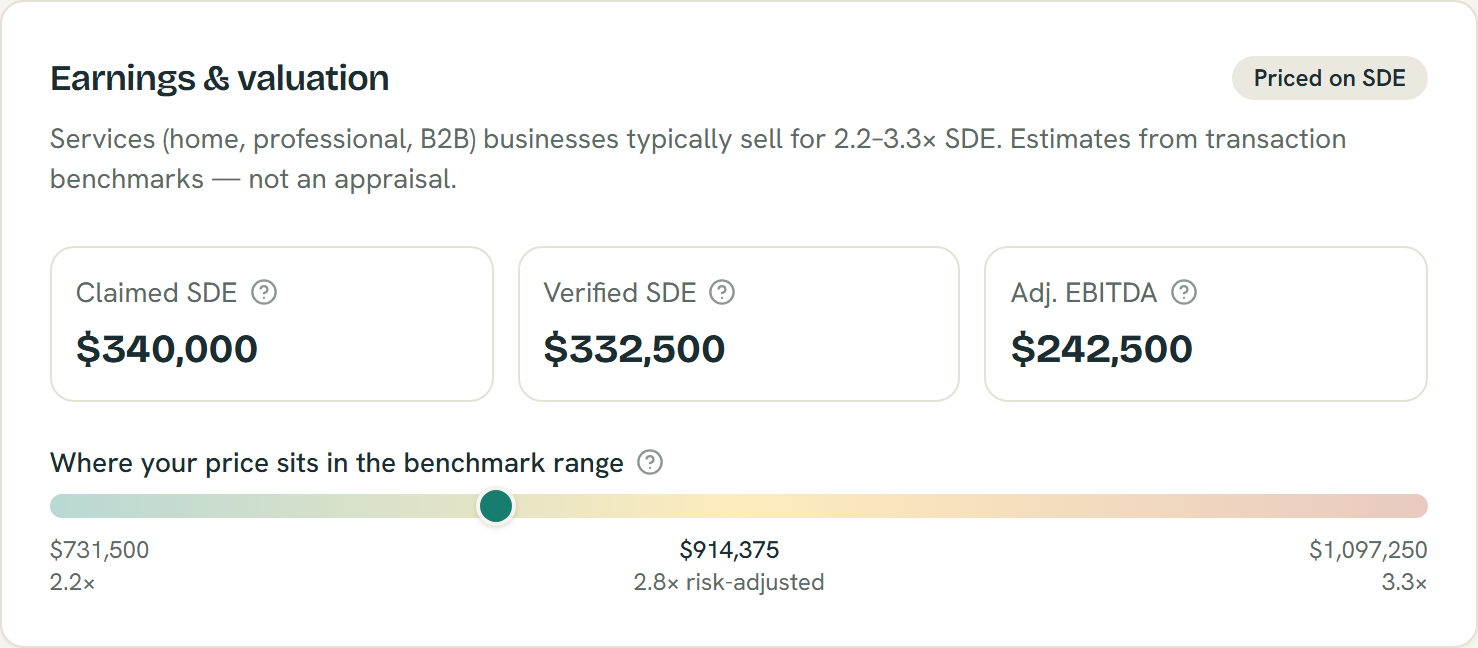

Claimed versus verified SDE and adjusted EBITDA, with the price placed on the industry multiple range — example data; an estimate, not an appraisal.

The transition zone

Between roughly $1M and $2M of earnings, both kinds of buyers show up — owner-operators pricing on SDE and small private-equity funds pricing on EBITDA — so businesses in that band should be modeled on both bases. Our Small Business analyzer does this automatically: it computes both figures, picks the right basis from the business's size and whether you'll operate it yourself, and shows both in the transition zone.

One more wrinkle: crossing from SDE pricing to EBITDA pricing can create value all by itself — that's the manager-hire play, and it's a big enough idea that it gets its own article.